Construction starts have remained robust this year but certain sectors could begin to see a slowdown in the coming months.

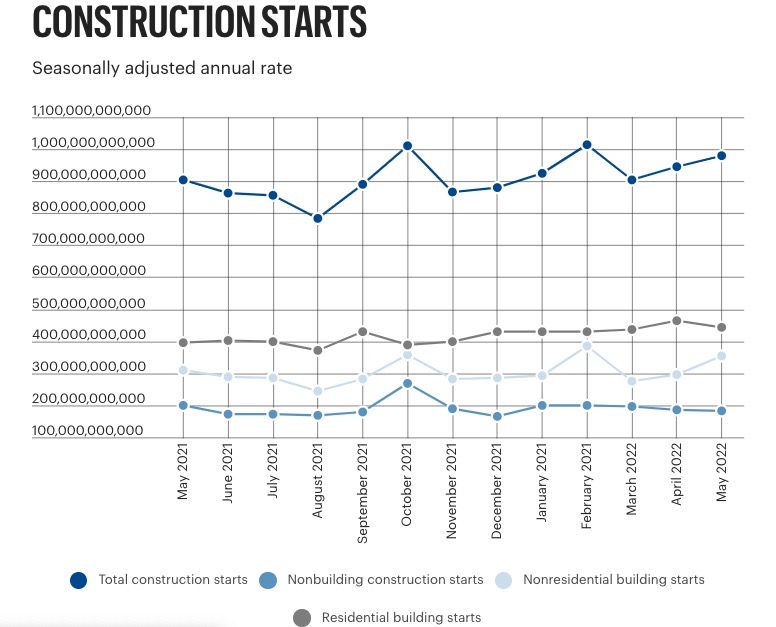

Total construction starts rose 4% in May to a seasonally adjusted annual rate of $979.5 billion, according to data released late last week by Hamilton, New Jersey-based Dodge Data and Analytics LLC. But among the major categories tracked by Dodge, nonresidential building starts was the only one that increased, by 20%, while residential starts fell by 4% and nonbuilding starts dropped 2% during the month.

It’s a signal homebuilders are starting to pull back on what had been an active construction pipeline through the Covid-19 pandemic, as demand for housing wanes amid a rising-interest-rate environment.

Year-to-date, total construction is 6% higher in the first five months of 2022 compared to the same period in 2021. In that period, residential starts have actually grown 3%, suggesting the tide is only starting to change on the homebuilding front.

Nonresidential building starts have increased 17% annually in the first five months of the year, while nonbuilding starts are 5% down.

Dodge didn’t respond by deadline for an interview request.

Richard Branch, chief economist at Dodge Construction Network, said in a statement the construction sector has become increasingly bifurcated in the past several months.

“Nonresidential building construction is clearly trending higher with broad-based resilience across the commercial, institutional and manufacturing spaces,” he said. “However, growth in the residential market has been choked off by higher mortgage rates and rapidly falling demand for single-family housing. Nonbuilding starts, meanwhile, have yet to fully realize the dollars authorized by the infrastructure act.”

Branch said while the overall trend in construction starts is positive, the very aggressive stance taken by the Federal Reserve to combat inflation risks slowing momentum in construction.

Ken Simonson, chief economist at the Associated General Contractors of America, said in an interview he felt homebuilders are in much more precarious position right now than multifamily or nonresidential construction.

Ripple effects on construction starts from the passage of the federal $1.2 trillion Infrastructure Investment and Jobs Act late last year hasn’t been felt yet. Simonson said for a while he’s expected contractors wouldn’t go to work on any IIJA-funded projects until late 2022 or early 2023, which he said he continues to expect. When that occurs, that’ll bolster the pipeline for the nonbuilding sector.

Outside of single-family home construction, multifamily and warehouse development — both of which have seen big growth through the pandemic — may be the most vulnerable to a slowdown, Simonson said.

Seattle-based Amazon.com Inc.’s (NASDAQ: AMZN) disclosure this spring that it had excessive warehouse capacity is one signal of slackening demand, he continued.

“Now that there’s doubt about how strong consumer demand is going to be for goods, I think other businesses are going to slacken their buying and building of warehouse space,” Simonson said.

Amid rising costs and interest rates, it’ll become more challenging for multifamily developers to pencil out deals, also making it more vulnerable than other sectors, he added.

One of the sectors likely to boom: manufacturing. New automotive plants, and large-scale facilities to support the burgeoning electric-vehicle industry, will translate to new business for general contractors nationally, Simonson said.

The largest nonresidential building projects to break ground in May were the $950 million Meta Platforms Inc. (NASDAQ: META) Hyperscale data center in Temple, Texas; the $940 million Digital Dulles data center in Dulles, Virginia; and a $540 million mixed-use building in New York, according to Dodge.

The Article is from Austin Business Journal, copyright belongs to owner