For high-net-worth investors and real estate owners, legally and efficiently deferring capital gains tax is a timeless pursuit. Within the U.S. tax code, the 1031 Like-Kind Exchange and Qualified Opportunity Zone (OZ) Funds stand out as the two premier tax-saving strategies.

Many investors find themselves at a crossroads. Some want to double down on real estate, while others seek to reduce their exposure to a single property asset class or gain immediate liquidity. To help you evaluate your options instantly, Real International has developed the comprehensive comparison framework below:

📖 For a comprehensive breakdown of each vehicle, feel free to explore our dedicated deep dives: “1031 Exchange: Buy Your Next Property Tax-Free!” and “Opportunity Zones: The Ultimate Real Estate Tax Strategy Guide.”

Below, we break down the 4 core mechanical differences behind the chart to guide your next strategic move.

What Are They Exactly?

Before diving into the mechanics, let’s quickly establish a clear, foundational definition for both tax shelters:

What is a 1031 Exchange? Simply put, it is a “property-for-property” swap. When you sell a commercial or investment property, as long as you reinvest the proceeds into another “like-kind” investment property within strict statutory windows, your capital gains tax is deferred and rolled entirely into the new asset.

What is an Opportunity Zone (OZ)? This is a federal tax incentive designed to stimulate economic growth in designated, distressed communities. When you realize capital gains from selling any asset (real estate, stocks, crypto, private business equity, etc.) and reinvest just the net profits into a qualified fund focused on development within these zones, the government rewards you with long-term tax deferral and tax-free wealth creation.

The 4 Core Mechanical Differences

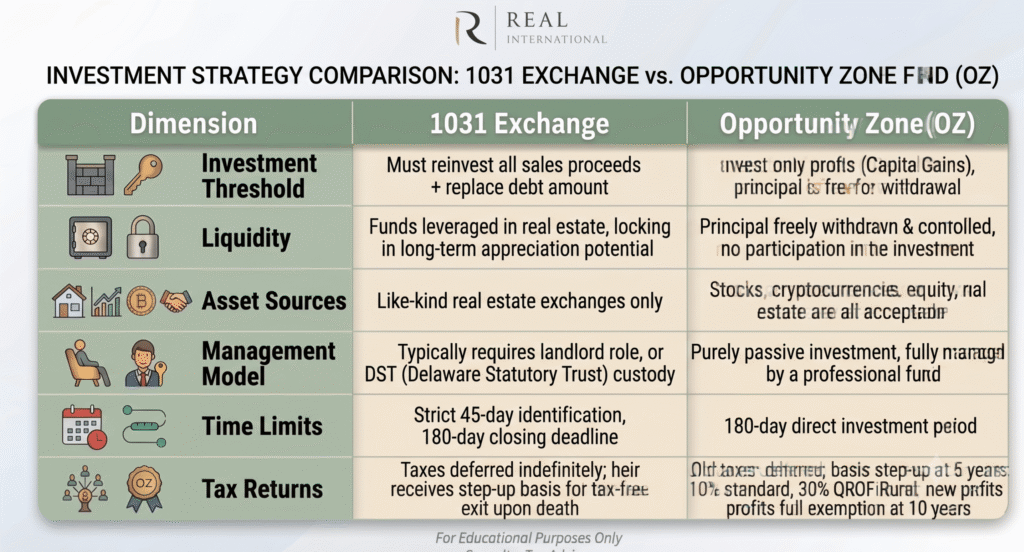

There is no single “perfect” tool, only the strategy that best aligns with your current wealth cycle. Let’s analyze their respective advantages across four critical dimensions:

01. Capital Reinvestment: Preserving Purchasing Power vs. Principal Liquidity

The Scale Advantage of 1031:If you sell a property for $2 million ($1.5M principal + $500K profit), a 1031 exchange requires you to reinvest the entire sale proceeds (both principal and profit) and replace any existing debt on the property. The massive advantage here is that your purchasing power and original asset scale remain completely intact. You can continue to use leverage on the full $2 million to acquire a larger property, giving the 1031 Exchange an absolute edge in compounding real estate wealth through market cycles.

The Flexibility of Opportunity Zones: OZs allow for the complete separation of principal and profit. Out of that $2 million sale, you only need to invest the $500K capital gain into the OZ fund. The remaining $1.5M principal can be kept entirely as liquid cash flow or deployed into other non-real estate investments. This is incredibly convenient for investors who want to pull cash out and avoid locking up 100% of their capital in fixed assets.

02. Asset Classes: Real Estate Exclusive vs. Cross-Asset Inclusivity

The 1031 Restriction: Reinvesting through a 1031 must satisfy the strict “like-kind” asset requirement, which under current law is exclusively limited to investment real estate for investment real estate. You cannot, for instance, roll profits from a stock portfolio or a business sale into real estate via a 1031.

The OZ Inclusivity: OZs accept capital gains generated from any asset class. Whether you sell physical real estate, public stocks, crypto, or private business equity, as long as it generates a capital gain, it qualifies for an OZ investment. This provides unparalleled diversification flexibility for investors looking to pivot across different asset classes.

03. Timelines: Precision and Rigidity vs. A High-Safety Plan B

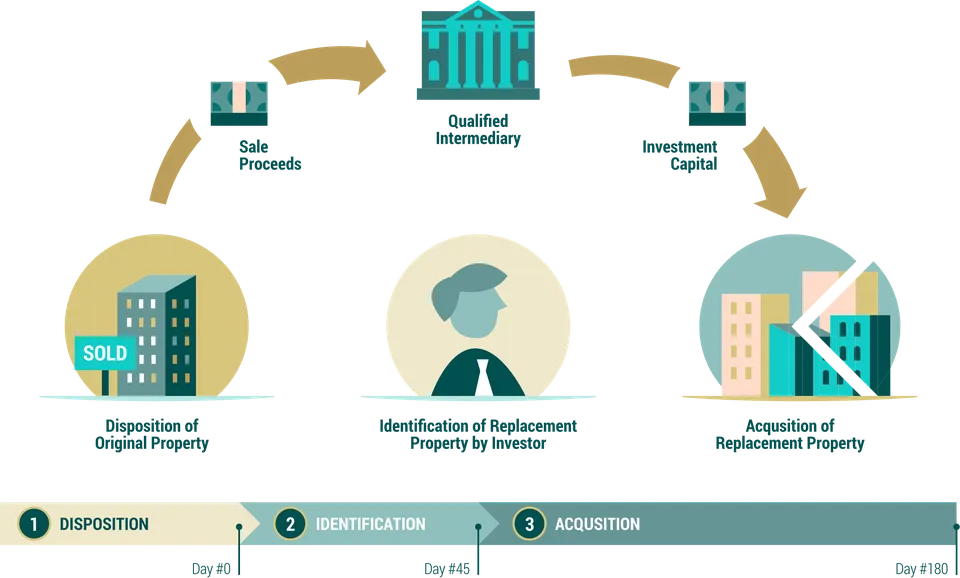

The Unyielding 1031 Timeline: You have a strict 45 days post-sale to formally identify the replacement properties in writing, and a strict 180 days to close escrow. There are virtually no exceptions to these deadlines.

The OZ Safety Net: OZs grant investors a 180-day window to deploy capital with zero pre-identification requirements. More importantly, in practice, an OZ fund serves as an excellent “Plan B” if a 1031 exchange fails. If your 45-day 1031 identification period lapses without finding a suitable property, you can quickly redirect your profits into an OZ fund before the 180-day mark, intercepting a massive tax bill right before it hits.

04. Tax Returns: Generational Tax Elimination vs. 10-Year Tax-Free Growth

This represents the most profound divergence in long-term financial planning, dictating how your family wealth legacy is structured. To evaluate the final tax return of these two strategies, we must first master a pivotal concept: the “Step-up in Basis.” In tax terms, your “basis” is your investment cost. A “step-up in basis” means the IRS artificially raises your purchase cost on the books. Because a higher book cost shrinks your taxable net profit, this is a massive tax-reduction benefit for investors.

1031 Exchange (Infinite Deferral and Ultimate Tax Elimination): By continually swapping properties, you can push your tax liabilities down the road indefinitely. If an investor holds the real estate portfolio until death, the heirs receive a 100% step-up in basis to the current fair market value. This means if the heirs sell the inherited portfolio at market value, their taxable profit drops to zero, effectively wiping out decades of accumulated, rolling capital gains taxes in a single stroke. However, a 1031 cannot offer tax-free gains on new investment profits realized during your lifetime.

Opportunity Zones (10-Year Holding, 100% New Profits Tax-Free): As long as you hold your capital in an OZ fund for at least 10 years, any and all new investment profits generated 100% permanently exempt from capital gains tax upon exit. It is critical to note, however, that your original deferred profit (the old tax liability) cannot be completely eliminated. It must eventually be paid by the federal statutory deadline.

- Under the updated OZ 2.0 legislation (effective for new investments moving into the 2027 structure), this original tax liability benefits from a phase-in cost basis step-up during the deferral period: investing in a Standard OZ project yields a 10% basis step-up , while investing in a newly established Rural Opportunity Zone Project (QROF) yields an impressive 30% basis step-up, substantially lowering your ultimate original tax bill.

![]()

💡 Real-World Case Study: Tired of Being a Landlord?

If you are facing a similar dilemma, look at how one of our actual clients navigated this: After selling a property, an investor allocated the original principal into stable, liquid cash-flow products, and rolling the capital gains into an OZ fund to minimize his physical property management headaches.

👉 Read the Full Case Study Here: “Done Being a Landlord: How One Investor Repositioned His Sale Proceeds for an 8% Yield and Tax-Free Growth“

Strategic Summary & Recommendations

Choose a 1031 Exchange if: You are a committed, long-term believer in physical real estate and want to maintain your existing asset scale and purchasing power. You plan to use leverage to continuously upgrade your portfolio and your ultimate goal is to pass a massive, unified real estate legacy to the next generation, completely eliminating all accumulated capital gains taxes upon transfer.

Choose an Opportunity Zone Fund if: You have a strong desire to ease the pressure of over-concentration in a single property. Alternatively, your gains originate from stocks, crypto, or a business sale rather than real estate, or you are facing an expiring 45-day 1031 identification window and urgently need a highly secure tax shelter. Just keep in mind that while the 1031 has the potential to eliminate your original tax liability through inheritance, an OZ fund will not eliminate that initial tax liability.

📍 Wondering which strategy perfectly aligns with your asset portfolio? Let’s connect today.