This article gives balanced, data-driven look at macroeconomic shifts and analyzes December leasing and sales activity across major areas in the Austin-Round Rock-San Marcos Metropolitan Statistical Area (MSA).

(Note: All housing market charts are sourced from Unlock MLS. Due to slight differences in reporting periods and geographic coverage, minor discrepancies in numbers may exist. Please focus on overall trends and market structure when interpreting these signals.)

Macroeconomic Snapshot

According to the latest reports, the U.S. Consumer Price Index (CPI) rose 2.7% year‑over‑year in December 2025, unchanged from November and in line with market expectations. The core CPI, which excludes food and energy, increased 2.6%, remaining within a moderate range.

Inflation has clearly receded from the highs of the past two years, but a quick return to the Federal Reserve’s 2% target remains unlikely. Economists point out that tariffs and essential goods prices continue to exert structural pressure on inflation, slowing the overall pace of disinflation.

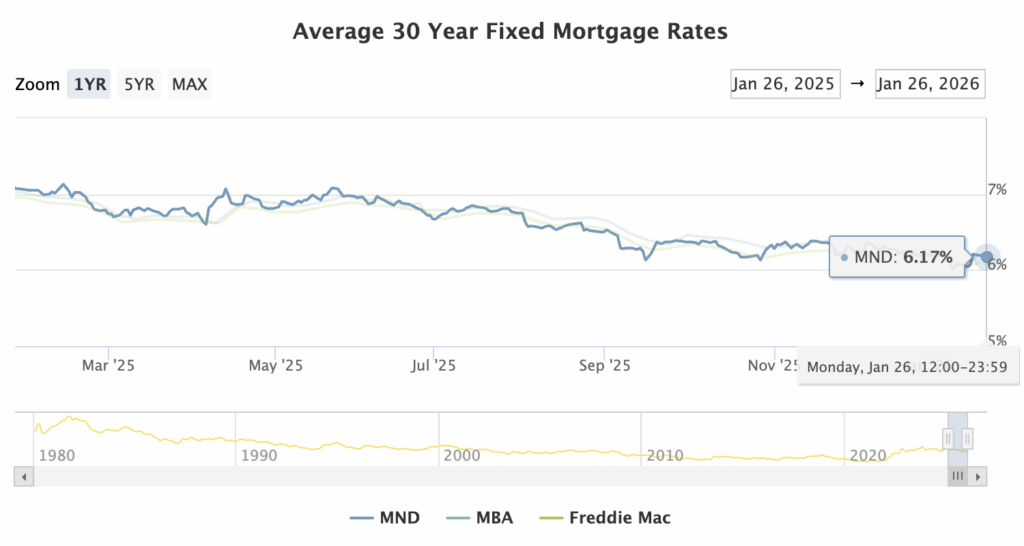

On the financing side, the 30‑year fixed mortgage rate hovered between 6.1% – 6.2%, showing limited short-term volatility. Recent policy uncertainty has made markets cautious about further rate declines, keeping borrowing costs from falling meaningfully.

Austin Metro Housing Landscape

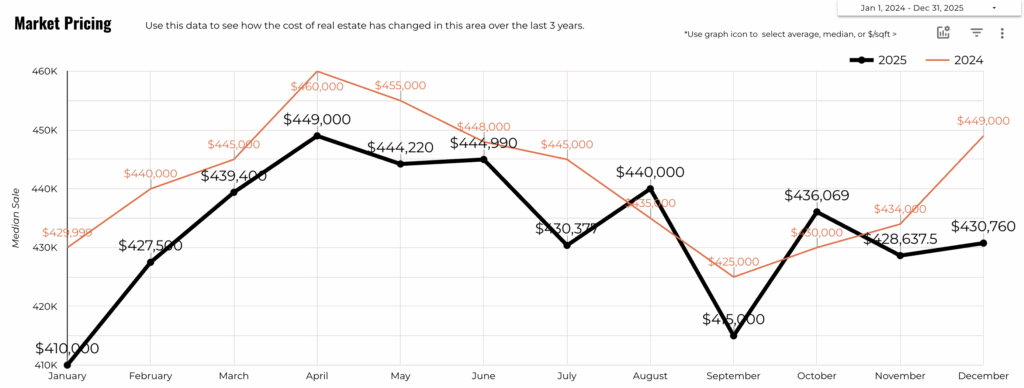

In December 2025, market activity across the Greater Austin area was slower than the previous year, yet home prices remained relatively steady. This indicates that sellers have not been resorting to large price cuts to stimulate transactions; instead, the market is working through inventory gradually under existing interest rate and supply‑demand conditions.

Transactional momentum still exists, though it now depends heavily on price alignment and property quality. Rather than steep declines, prices are seeing measured adjustments, helping sustain a steady flow of sales while maintaining overall market stability.

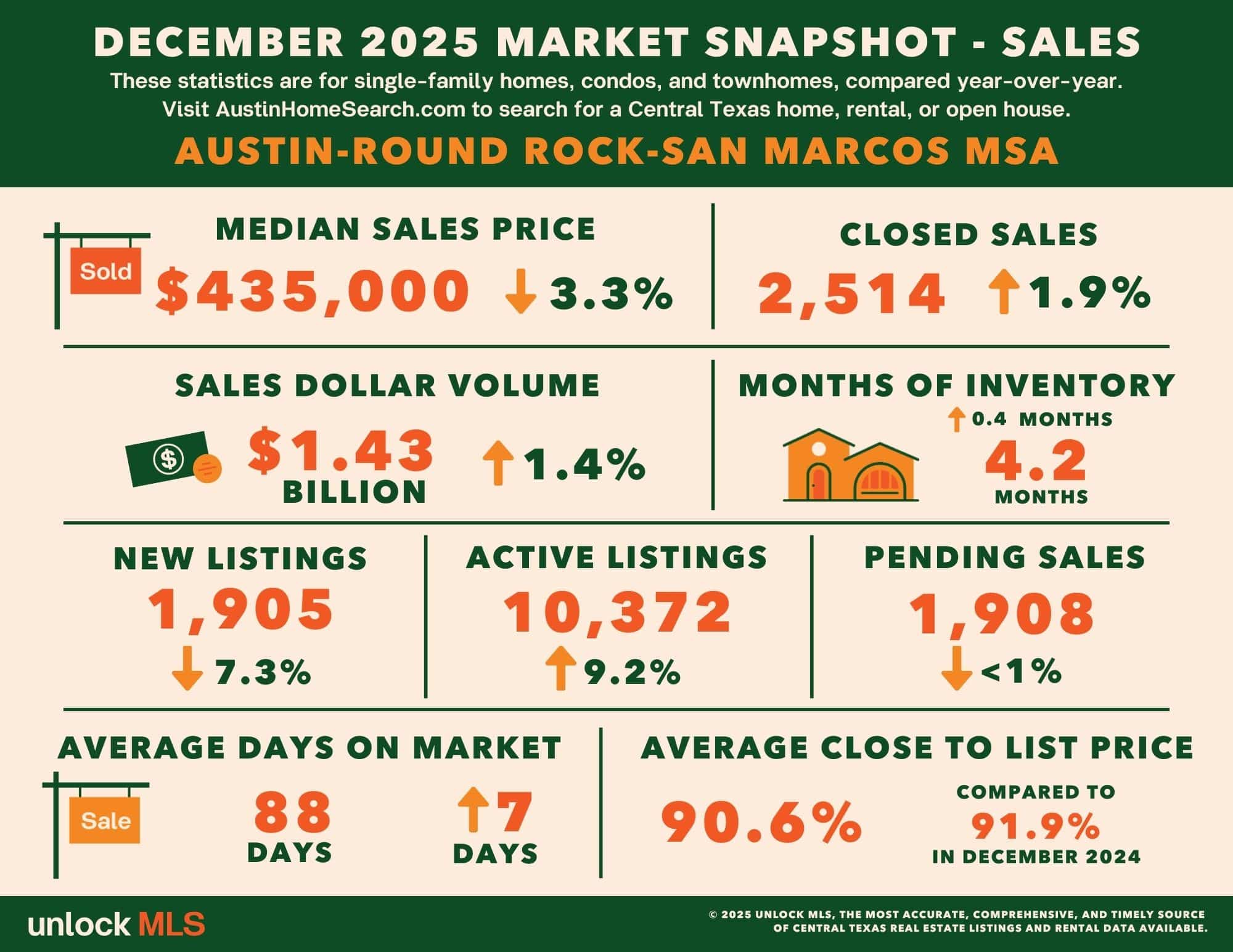

Pricing and Sales Activity

The broader Austin metro area reported a median home price of $435,000 in December, down 3.3% year‑over‑year. Despite the continued price correction, closed sales increased 1.9% to 2,514 units, while total transaction volume edged up 1.4% to $1.43 billion.

Pending sales stood at 1,908 units, nearly flat from a year ago, suggesting that buyer momentum remains cautious as many await clearer signals on mortgage rates and affordability.

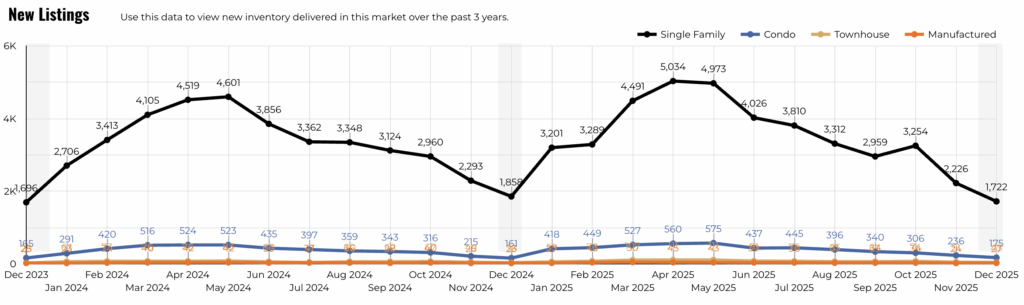

Listings and Inventory

New listings across the Austin metro reached 1,905 units, down 7.3% year‑over‑year. This indicates that some sellers are holding back, waiting for more favorable conditions before entering the market.

However, active listings increased 9.2% to 10,372 units, keeping inventory elevated. Months of inventory rose to 4.2 months, noticeably higher than last year’s levels, a sign that supply pressures persist even as demand remains selective.

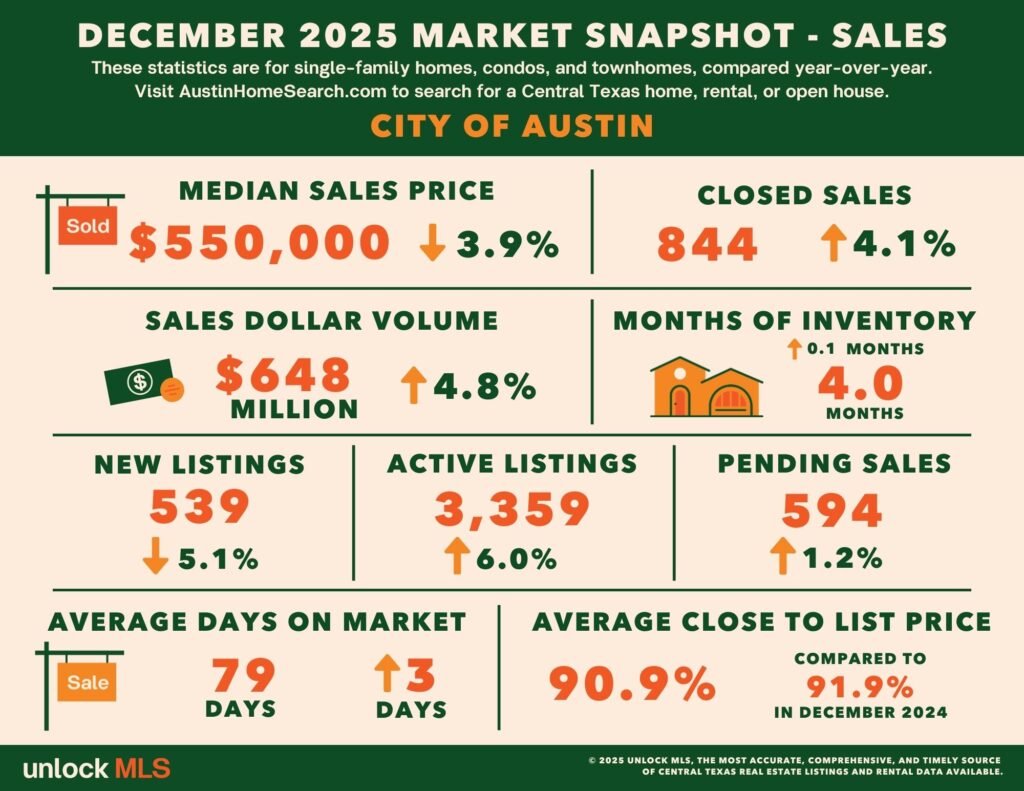

At the city level, Austin proper showed stronger activity: closed sales rose 4.1%, total sales volume up 4.8%, while the median price declined 3.9% year‑over‑year.

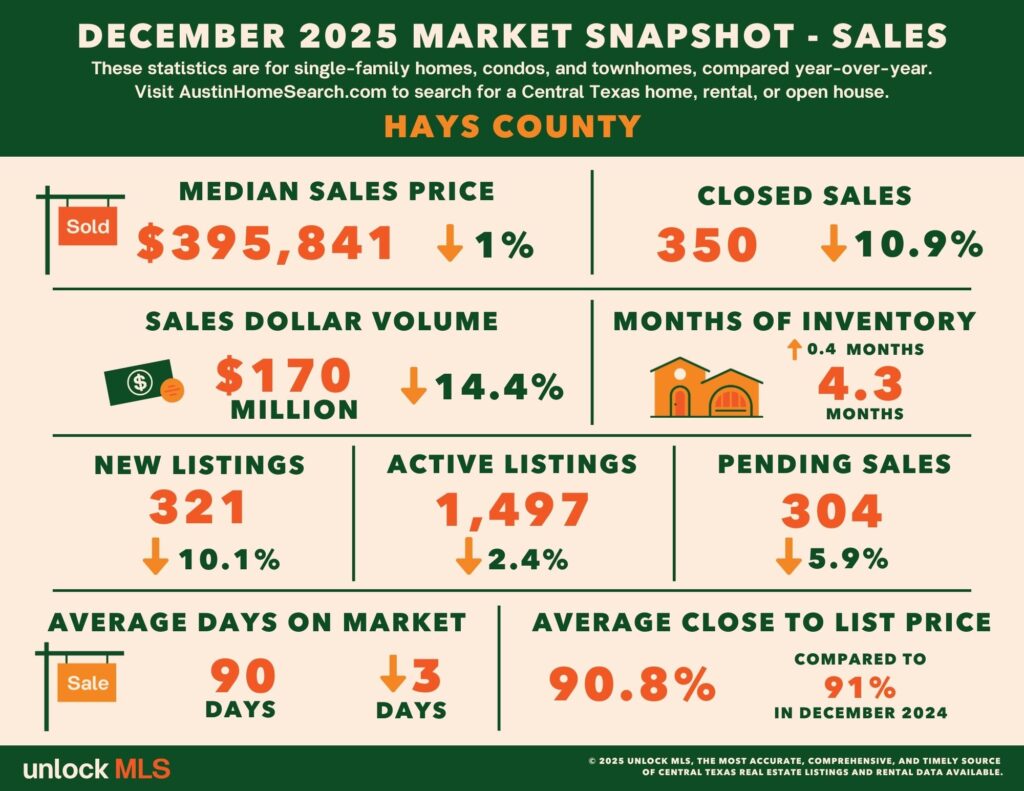

In contrast, outlying counties experienced different dynamics. For example, Hays County recorded a 10.9% drop in transactions, but only a 1% dip in median price. This suggests that buyers are focusing on fairly priced, higher‑quality listings, leaving limited options in the active market.

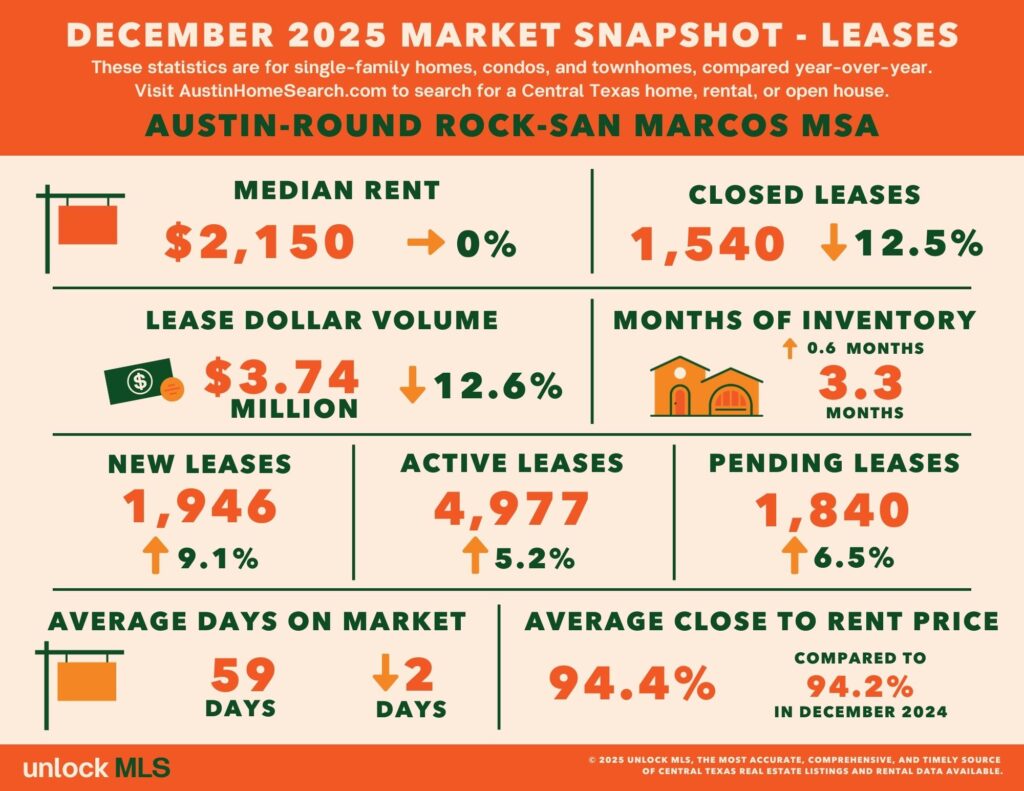

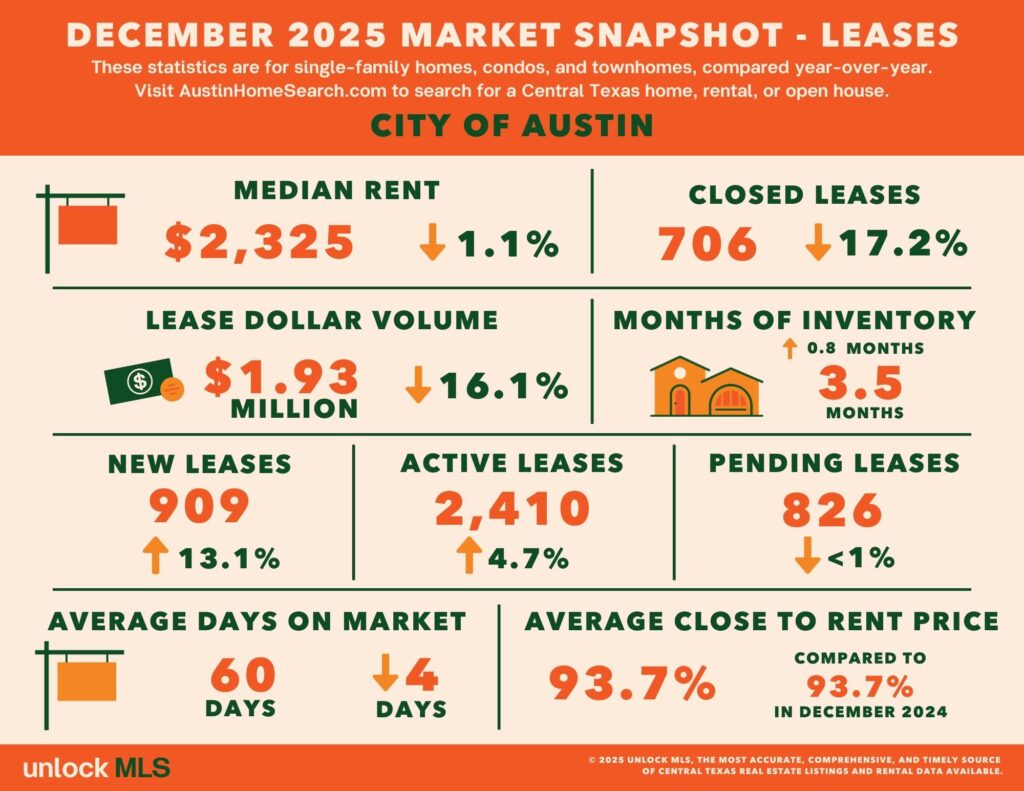

Rental Market

The Austin metro rental market remained price‑stable but less active. Total lease activity fell about 13% year‑over‑year, while median rents held steady compared with December 2024.

This pattern shows that despite increased supply, landlords are not cutting rents aggressively to drive occupancy. Instead, renters are taking longer to make decisions, resulting in slower leasing cycles.

In Austin city proper, the trend was even more pronounced: median rent slipped 1% to $2,325, while lease transactions dropped 17.2% from a year earlier.

A large volume of newly delivered apartments continues to weigh on the market. Once this wave of multifamily supply is absorbed, and deliveries slow, the single‑family rental segment is expected to regain momentum in subsequent quarters.

Takeaways for Buyers and Sellers

For Buyers: The upcoming spring 2026 market is likely to offer more favorable conditions. Nevertheless, well‑priced homes in desirable locations still sell quickly. Preparing early in Q1 can help you secure a stronger position before competition intensifies in spring.

For Sellers: Although prices remain relatively stable, listings continue to accumulate. If you plan to sell this spring or early summer, now is the time to prepare. In 2026, pricing strategy and presentation quality will matter more than in recent years. With realistic pricing and clear marketing plans, motivated buyers are still active and ready to make deals.

If you’d like a deeper dive into specific submarkets or are considering buying, selling, or investing, feel free to reach out. Real International is here to help you navigate the market with tailored insights and strategy.

📧info@realinternational.com