The Emerging Trends in Real Estate® 2026 report, jointly published by PwC and the Urban Land Institute, is widely recognized as one of the most influential annual outlooks in the U.S. real estate industry. Drawing insights from fund managers, developers, operators, lenders, brokers, consultants, and institutional investors, the 139-page report provides a comprehensive view of how industry participants interpret capital markets, development cycles, consumer demand, and the evolving structure of American cities.

Below, Real International distills the most important takeaways for investors.

Five Major Real Estate Trends for 2026

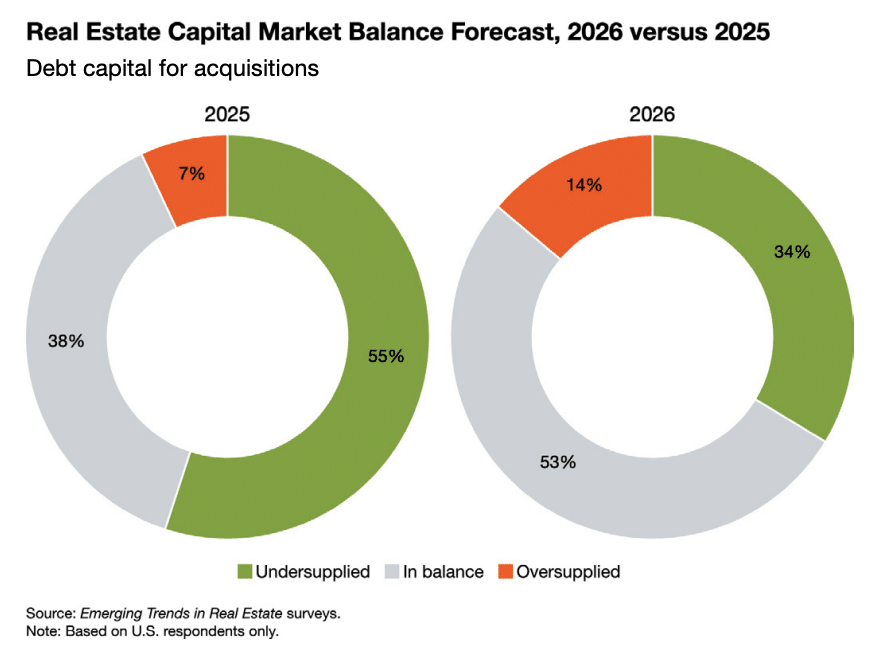

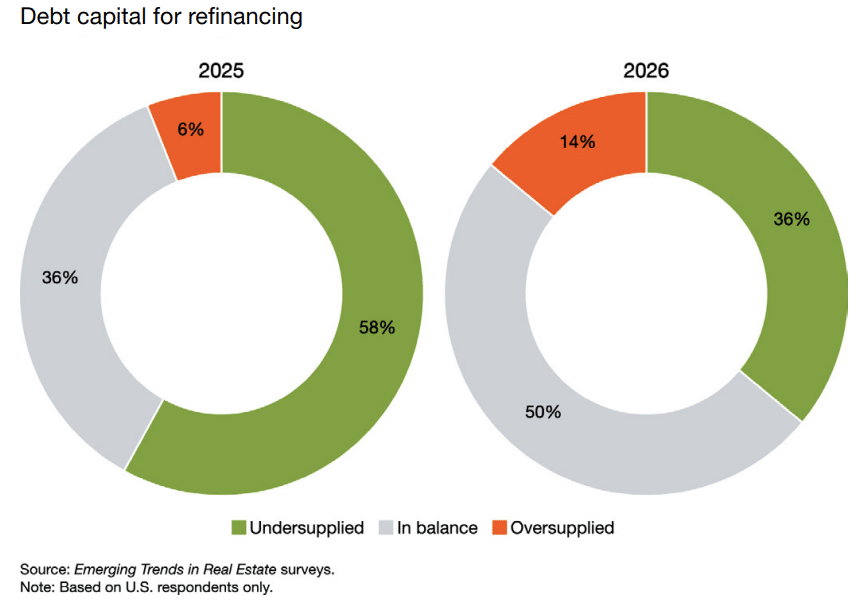

01. Capital Markets Remain in a Fog of Uncertainty

The capital environment heading into 2026 is shaped by one defining theme: uncertainty, especially around interest rates and the cost of debt. Liquidity has improved from the immediate post repricing period, but lenders remain selective, and many investors expect tight credit conditions to persist for both acquisitions and refinancing.

This backdrop is pushing refinancing risk higher and keeping transaction volume subdued. Strategy is rotating away from relying on cap rate compression and toward resilient income, conservative leverage, and disciplined underwriting, with a focus on durable cash flow rather than financial engineering.

02. Niche Assets Move Into the Mainstream

With confidence shaken in certain traditional sectors, especially office and parts of the multifamily market, capital is gravitating toward asset types supported by long-term structural demand.

Data centers stand out as a pure supply-demand imbalance story, constrained by power availability and suitable land. Student housing continues to benefit from enrollment growth, extremely high occupancy, and limited new supply. These factors have made both categories increasingly attractive to institutional capital.

Across the industry, niche assets are no longer viewed as portfolio supplements. They are becoming part of the core allocation. At the same time, performance can vary widely across markets, and investors must evaluate each city’s demographic and supply dynamics individually.

03. Back to basics: Where Analytics Meet Operations

With construction, financing, and labor costs all elevated, an asset’s NOI resilience and operational capability are becoming primary determinants of performance. Competitive properties are those with strong tenant retention, compelling amenities, and efficient, digitally enabled building systems.

Investment decisions are also becoming more granular. Instead of “picking the right city,” investors are increasingly focused on submarkets, micro-locations, and operational quality, small differences that increasingly drive meaningful variance in returns.

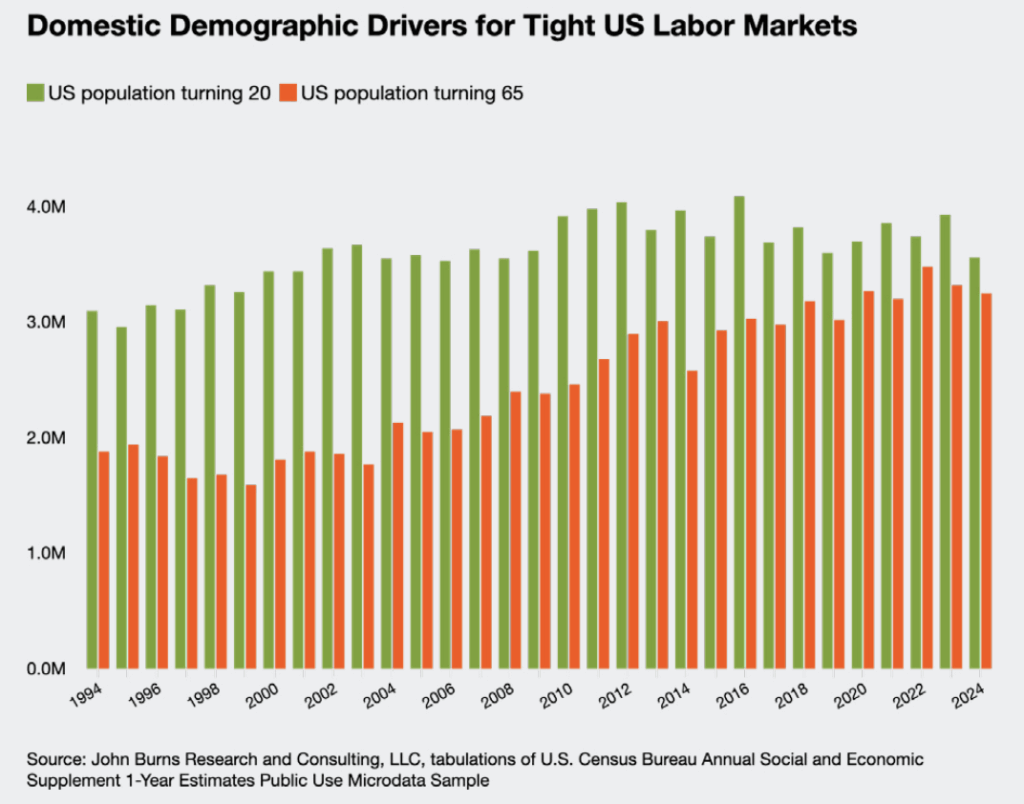

04. Demographic Shifts Reshape Long-Term Demand

Demographics remain the most reliable long run driver of real estate demand. U.S. population growth is increasingly reliant on net international migration, while domestic migration continues to favor Sun Belt and select “Snow Belt” markets that offer affordability, jobs, and quality of life.

Delayed household formation is extending the renter phase and creating future housing demand, while the rapidly growing 80 plus population supports long term need for senior housing and healthcare real estate. These trends point toward strategies anchored in population flows and age structure, not short term sentiment.

The gap between the number of people in the United States turning 20 each year and those turning 65 is gradually narrowing.

The gap between the number of people in the United States turning 20 each year and those turning 65 is gradually narrowing.

05. AI Becomes Fully Embedded in Real Estate Operations

The report describes 2026 as the year AI becomes truly “operationalized.”

Instead of being a tool used in isolated workflows, AI is becoming part of integrated property-wide systems, supporting lease management, energy monitoring, predictive maintenance, tenant communication, and even investment decision-making.

Assets equipped with advanced digital infrastructure are increasingly viewed as more controllable, more efficient, and ultimately more valuable. Operational technology is becoming part of the underwriting process, not an afterthought.

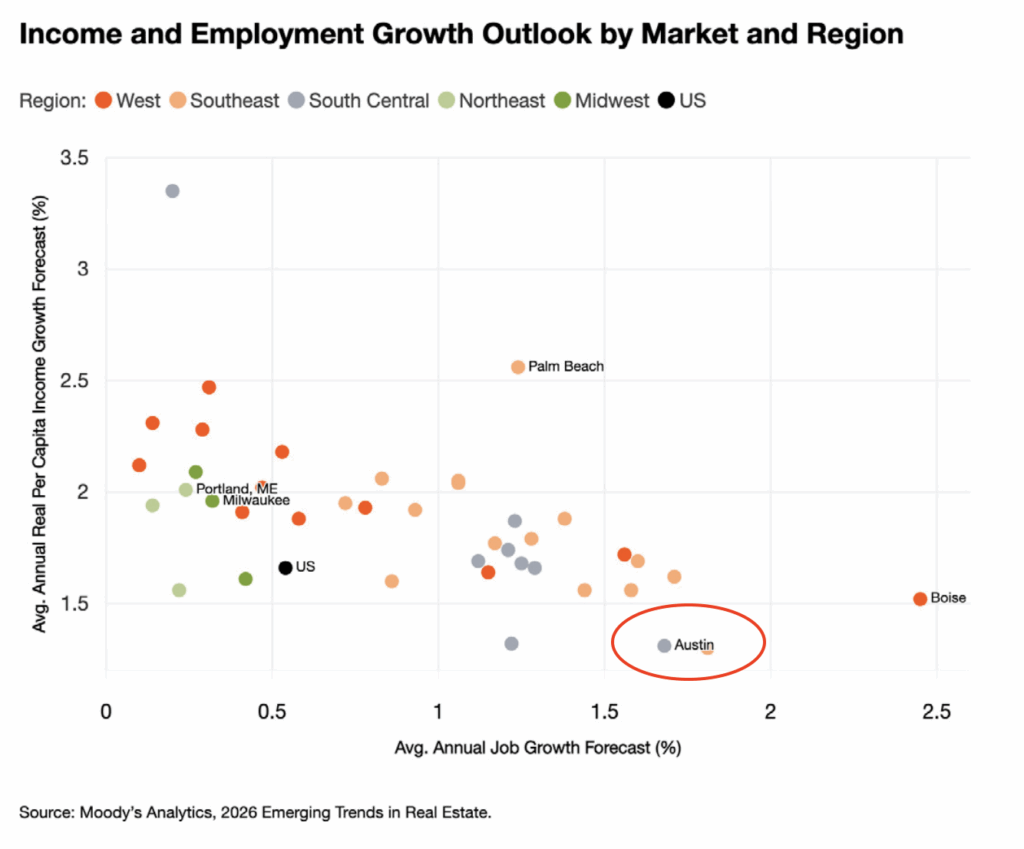

Texas Market Outlook: A Region of Diverging Strengths

Across Texas, the report highlights shared tailwinds but different local strengths and risk profiles.

Dallas–Fort Worth benefits from corporate relocations, diversified employment, and its role as a logistics and services hub.

Houston is supported by its energy, healthcare, and industrial base, even as office performance remains uneven.

San Antonio offers relative affordability and steady household growth, appealing to income‑oriented investors.

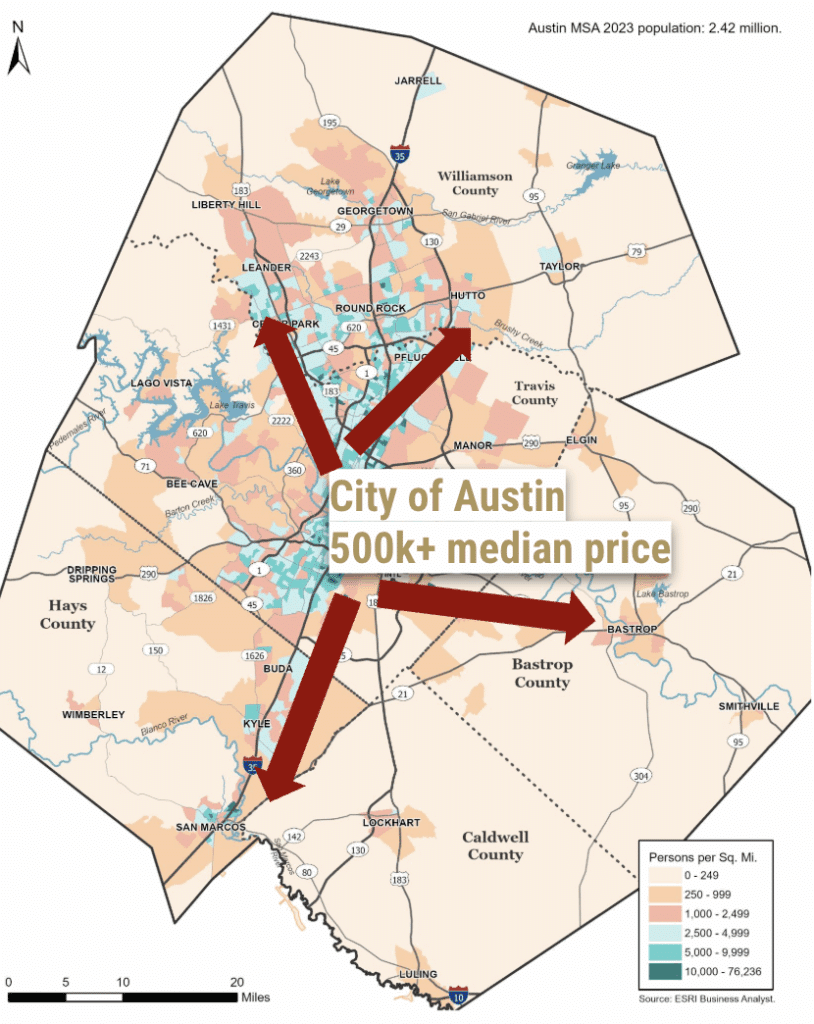

Austin combines a deep tech ecosystem, high skilled workforce, and strong job growth prospects. Although a sizable multifamily pipeline, roughly 4–5 percent additional inventory in 2026–2027, may weigh on near term rent growth, it can also create a more attractive entry point for long term capital.

Migration patterns reinforce this picture. Households continue to move from high cost coastal markets into more affordable Sun Belt metros, including Texas. Within the Austin area, demand is increasingly dispersing toward suburban centers such as Buda, Kyle, Manor, and Leander, as families seek better affordability, schools, and community infrastructure, gradually shaping a more polycentric region.

2026: A Year Defined by Structural Divergence

Rather than broad strength or weakness, 2026 is likely to be defined by structural divergence across asset types, metros, and submarkets. Demographics, technology, supply cycles, climate and policy risk, and operational execution will increasingly drive performance gaps.

In an uncertain market, long‑term returns are more likely to come from structural trends than from chasing short‑term momentum, by focusing on markets where demand is resilient and new supply is disciplined.

If you would like a clearer view of how to position in today’s environment, feel free to connect with us.

📧info@realinternational.coom