This article gives balanced, data-driven look at macroeconomic shifts and analyzes February leasing and sales activity across major areas in the Austin-Round Rock-San Marcos Metropolitan Statistical Area (MSA).

(Note: All housing market charts are sourced from Unlock MLS. Due to slight differences in reporting periods and geographic coverage, minor discrepancies in numbers may exist. Please focus on overall trends and market structure when interpreting these signals.)

Macroeconomic Snapshot

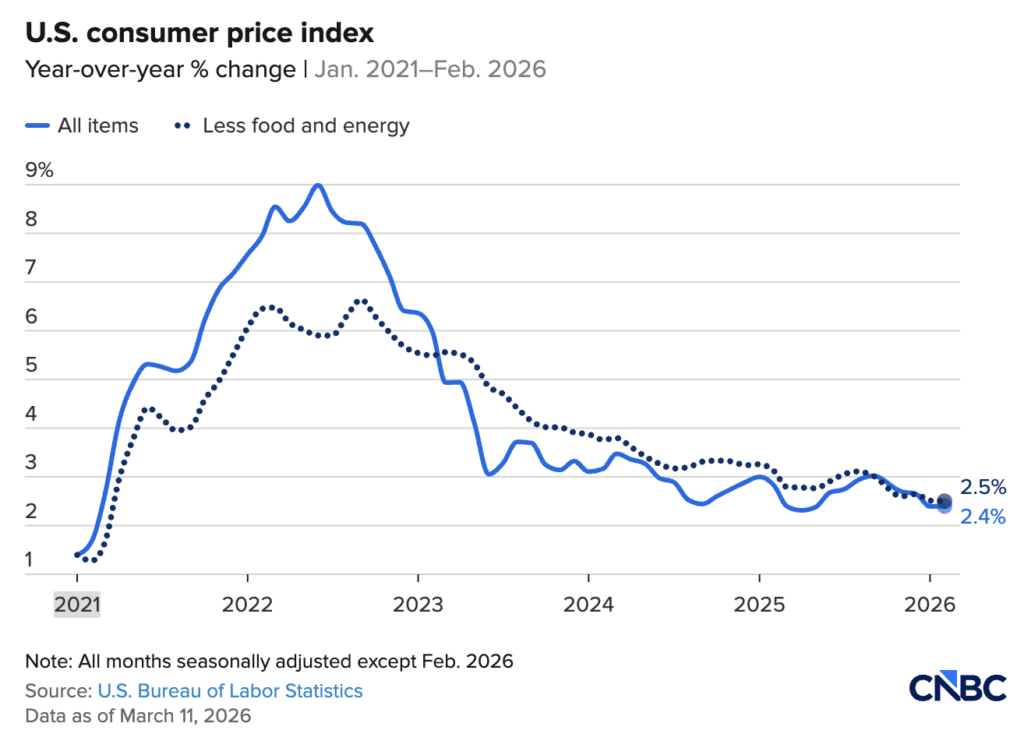

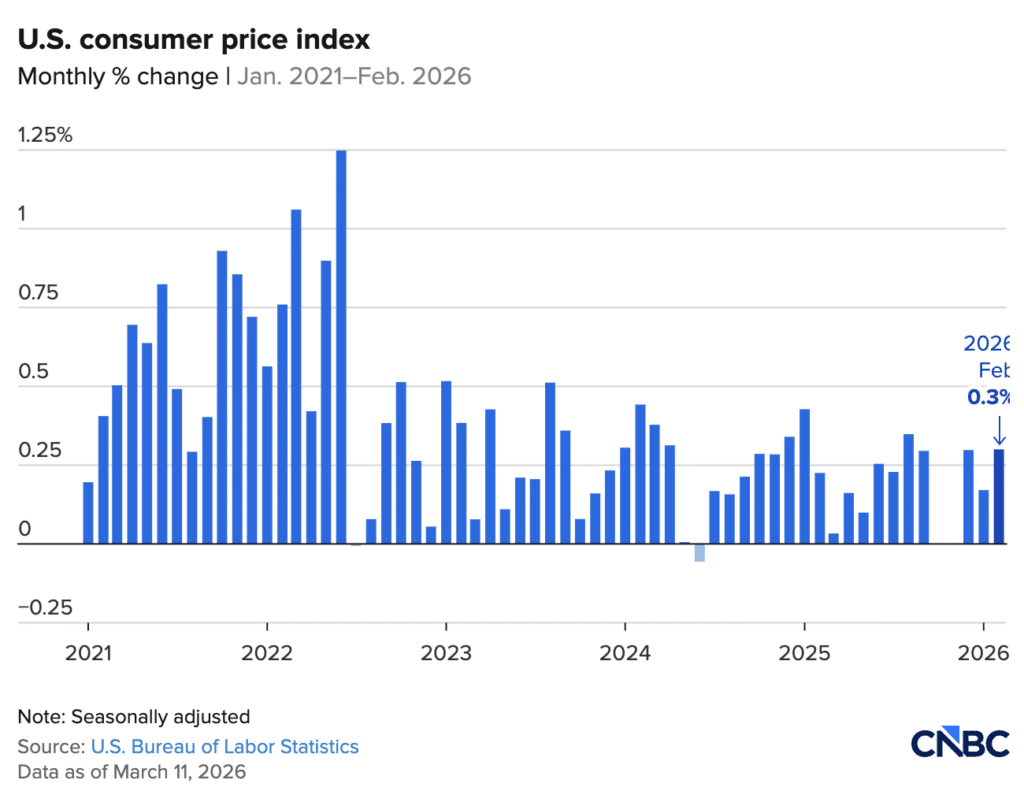

According to the latest release, the U.S. Consumer Price Index (CPI) rose 2.4% year-over-year in February 2026, unchanged from January and in line with expectations. While inflation remains slightly above the long-term target, the overall downward trajectory continues.

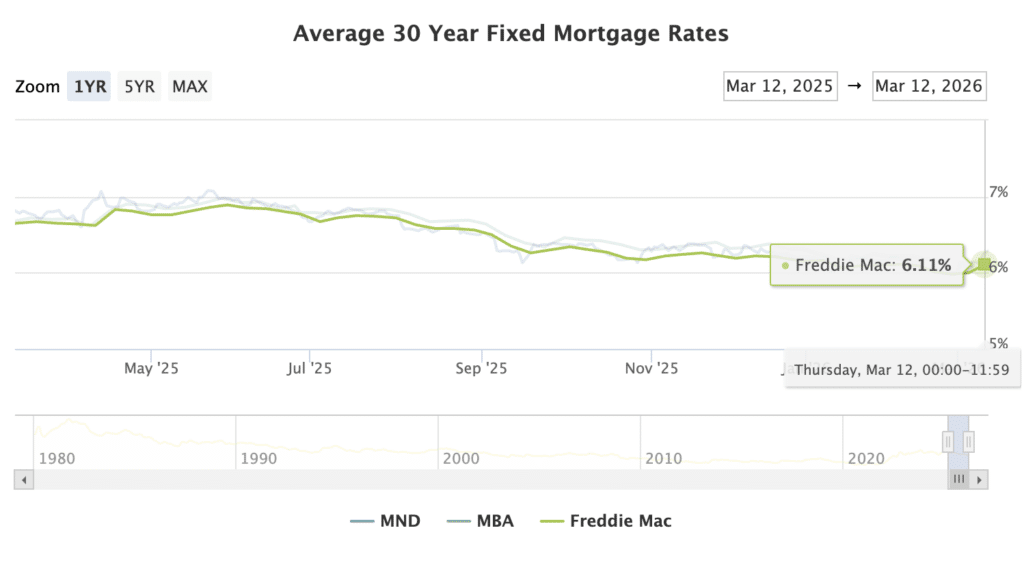

From a policy standpoint, the Federal Reserve maintains a conservative short-term stance even though its long-term path toward rate cuts hasn’t changed. Amid recent geopolitical tensions, 30-year fixed mortgage rates rebounded slightly to around 6.11%.

Despite this minor uptick, mortgage rates remained relatively stable throughout February — and Austin’s homebuyers didn’t waste that window of opportunity.

As John Crowe, 2026 Unlock MLS and ABoR President, explained:

“Many buyers have spent the past year waiting to see where prices would go. Conditions now look more favorable for buyers to act. With real-time MLS data and professional guidance, they can make decisions based on facts, not headlines.”

Austin Metro Housing Landscape

February typically marks a turning point when Austin’s housing market shifts from winter slowdown to spring revival. While transaction volume remained somewhat soft due to seasonal effects, several leading indicators suggest demand is warming up.

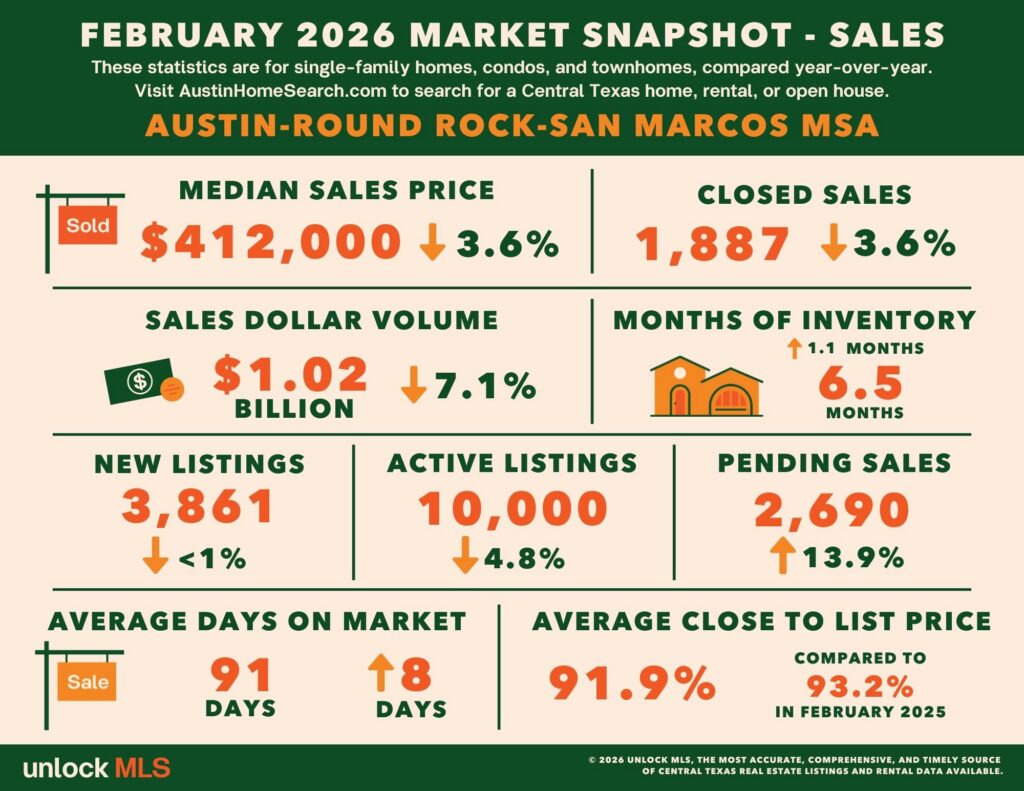

The average close to list price ratio rose from 90.6% in December to 91.9% in February, suggesting stronger alignment between buyers and sellers. Pending sales rose 13.9% year-over-year to 2,690 transactions, showing faster buyer return.

Pricing and Sales Activity

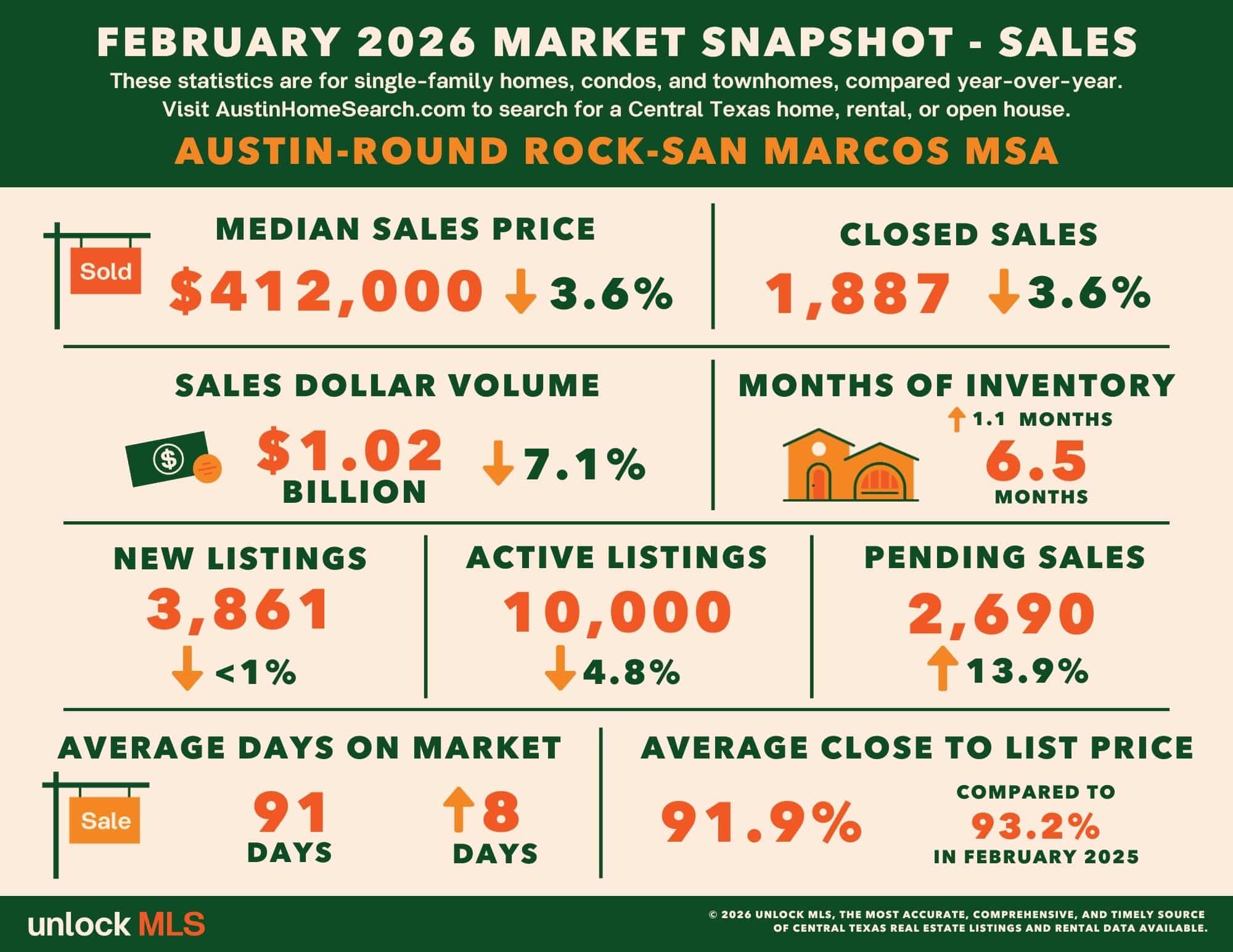

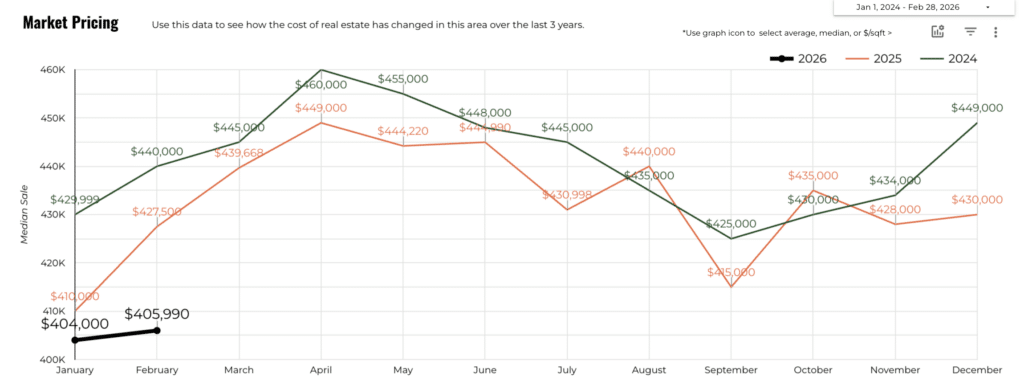

Across Greater Austin Area, the median home sale price in February reached $412,000, down 3.6% year-over-year. The price trend line for 2026 shows a gentle upward curve between January and February, signaling that Austin’s spring homebuying season has officially begun.

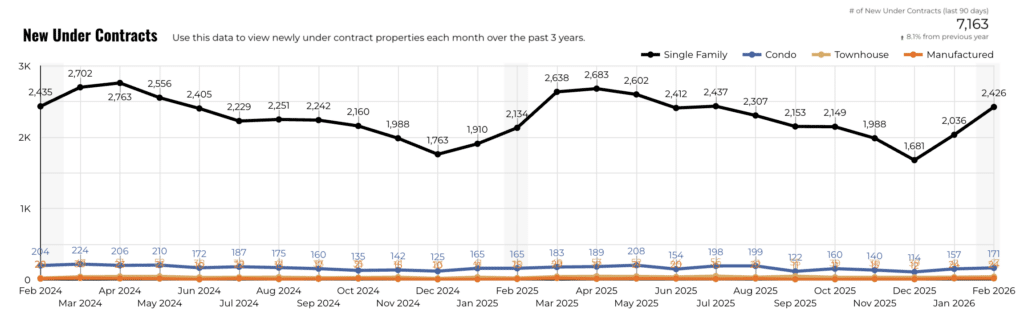

A key data point this month was pending sales, which jumped 13.9% year-over-year to 2,690 transactions. The sharp increase shows that buyers are moving early, a sign of growing market confidence heading into spring.

Listings and Inventory

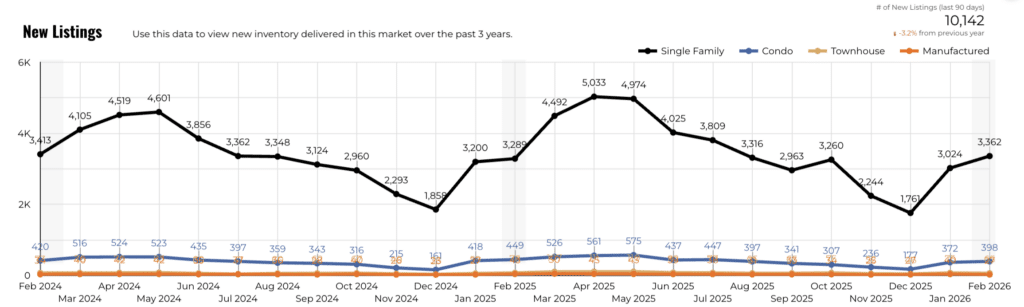

New listings in February totaled 3,861 units, down slightly (less than 1%) from the previous year. Active listings stood at 10,000, a 4.8% year-over-year decline.

While buyers are clearly returning, new supply remains steady, leading to faster inventory absorption. The current months of inventory sits at 6.5 months, which still characterizes a buyer’s market, but tightening conditions are reducing downward pressure on prices.

Regionally, the trend is consistent: moderate pullbacks in closed sales, but a strong surge in new contracts.

Austin city proper saw its median price dip 2.7% to $540,000, yet pending sales climbed 15.1%. Core-area demand is rebounding most noticeably, premium locations remain the market’s anchor.

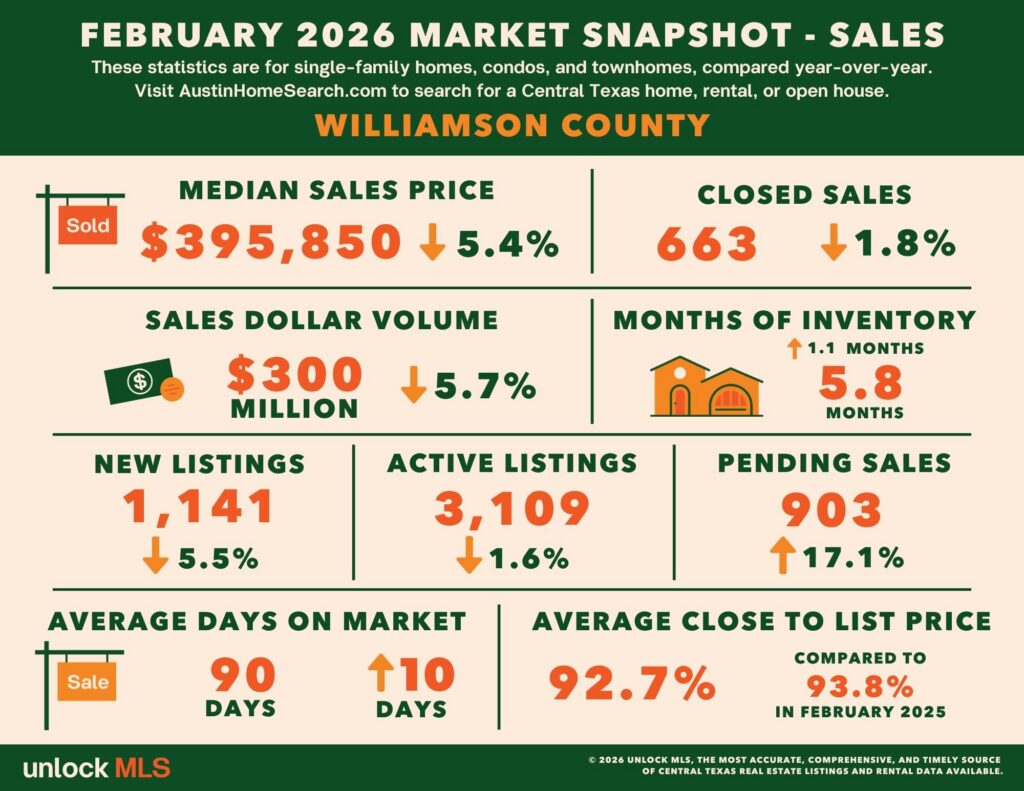

Williamson County stood out with a 17.1% jump in pending sales, even with a modest price pullback. Buyer enthusiasm in the northern suburbs has returned early, setting up a competitive spring.

Rental Market

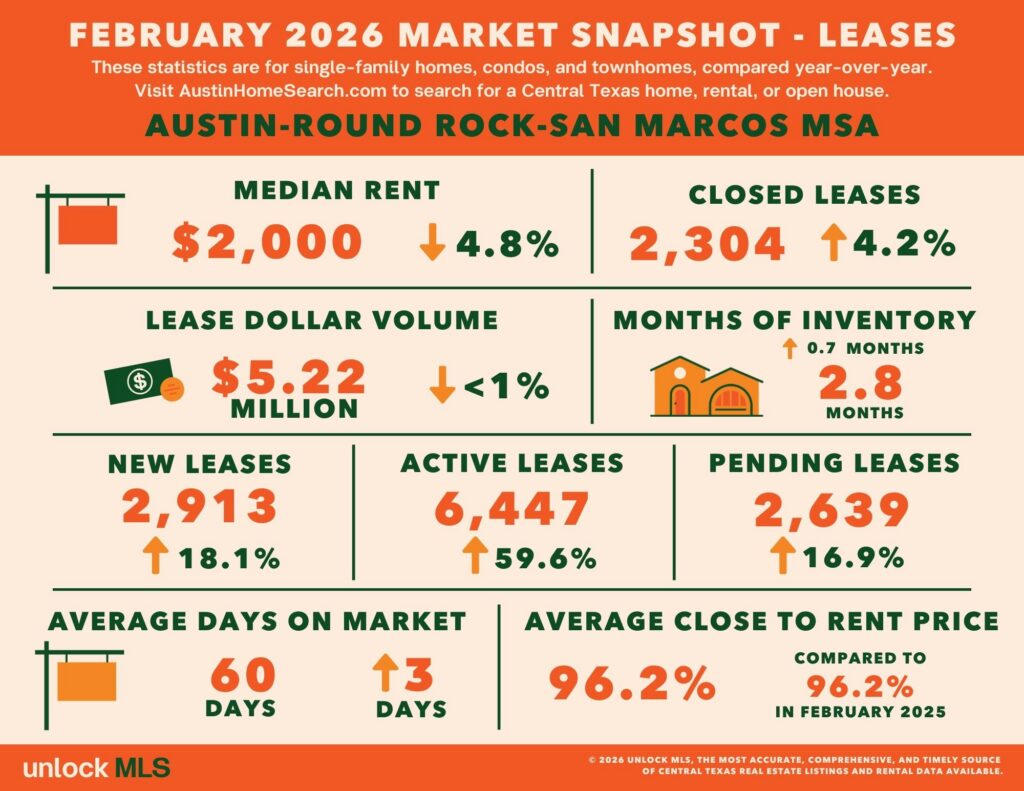

In February, the Greater Austin rental market continued to face heavy inventory pressure. The median rent fell to $2,000, down 4.8% year-over-year, while lease closings rose 4.2%.

Despite rising transaction volumes, the surge in available rentals, up 59.6% from a year earlier, keeps the market firmly in oversupply.

Competition among landlords is intensifying. New rental listings rose 18.1%, meaning more properties are hitting the market just as the spring leasing season begins.

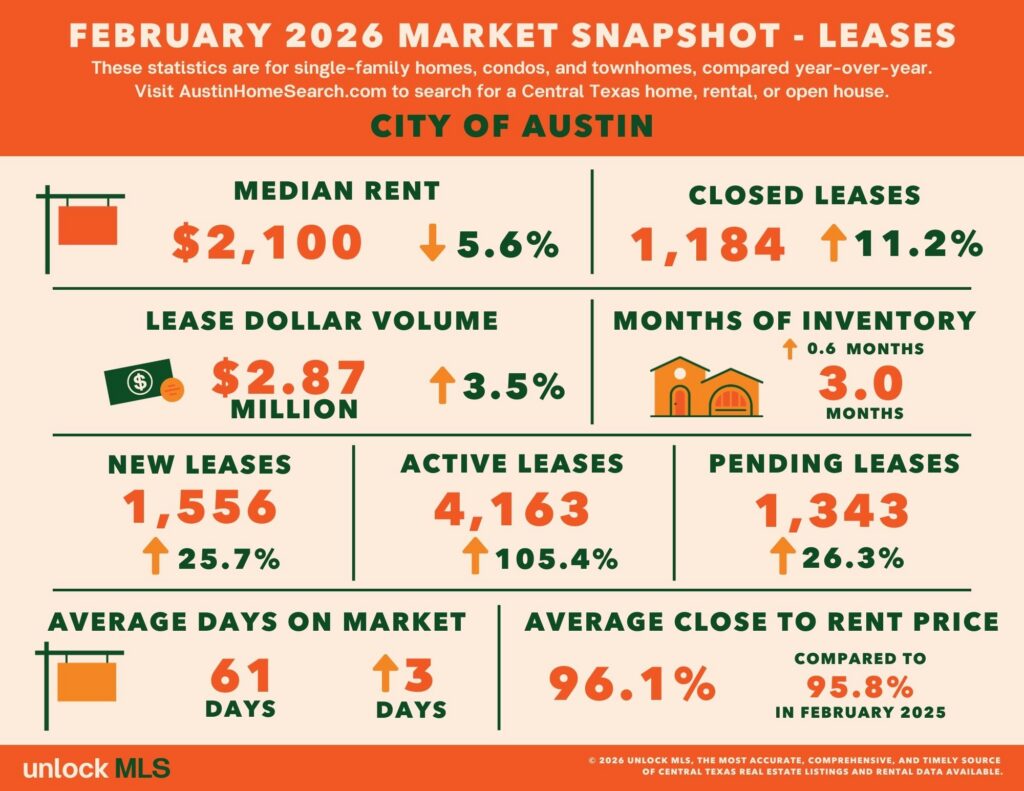

Within Austin city, the situation is even more pronounced. Active rental inventory doubled, soaring 105.4%, largely due to a wave of newly delivered apartment complexes and some unsold listings shifting from “for sale” to “for rent.”

This dual influx of supply continues to pressure rental prices and extend leasing timelines, especially in the urban core.

Insights for Buyers and Sellers

For buyers:

Take advantage of the current price and negotiation window. The market still favors buyers with high inventory and softer prices, even as competition quietly builds. Rather than wait for lower rates that could trigger bidding wars, now is an ideal time to lock in deals before demand heats up.

For sellers:

Pricing strategy is everything. The market is gaining strength, but buyers remain price-sensitive. Well-presented homes priced accurately can still sell quickly. Spring’s active season offers a prime opportunity to capture motivated buyers before summer inventory surges.

If you’d like a deeper dive into specific submarkets or are considering buying, selling, or investing, feel free to reach out. Real International is here to help you navigate the market with tailored insights and strategy.

📧info@realinternational.com