This article gives balanced, data-driven look at macroeconomic shifts and analyzes November leasing and sales activity across major areas in the Austin-Round Rock-San Marcos Metropolitan Statistical Area (MSA).

(Note: All housing market charts are sourced from Unlock MLS. Due to slight differences in reporting periods and geographic coverage, minor discrepancies in numbers may exist. Please focus on overall trends and market structure when interpreting these signals.)

Macroeconomic Snapshot

Based on the latest release, U.S. consumer inflation continued to ease in November. Headline CPI rose 2.7% year over year, below the market expectation of 3.1%, extending the broader trend of gradual cooling seen over the past year. Core CPI, which excludes food and energy, increased 2.6%, also coming in below expectations and indicating that inflation pressures are moderating in a more balanced way.

Because October CPI data was unavailable, November’s report should not be interpreted as a single inflection point. That said, the overall direction has become clearer: inflation is putting less pressure on interest rates than it did earlier in the cycle.

Shelter costs, which are particularly relevant to the housing market, rose about 3% year over year. While shelter remains a persistent component of inflation, its growth pace has slowed meaningfully relative to the highs of the past two years, indicating housing-related inflation is easing gradually.

Financing conditions remain incremental in improvement. The latest data place the 30-year fixed mortgage rate around 6.2%, still high by historical standards. As a result, many buyers remain cautious, and transaction decision timelines continue to stretch.

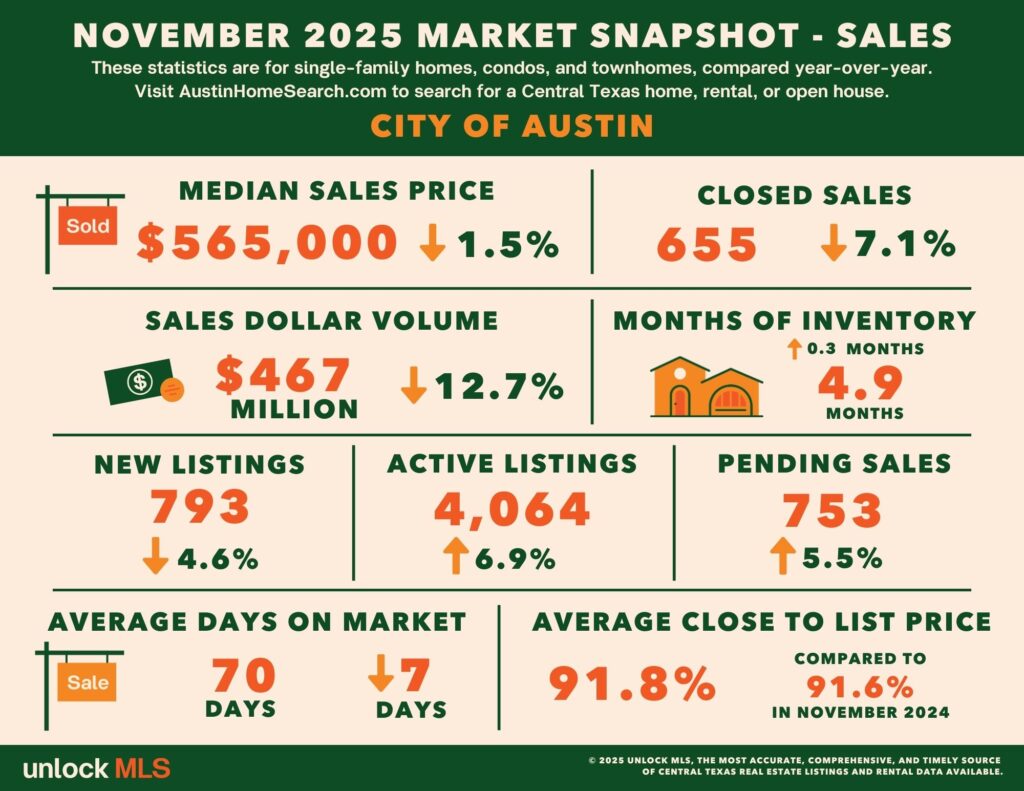

Austin Metro Housing Landscape

Entering November, housing activity across the Austin metro area slowed versus a year ago, while price adjustments remained limited. This dynamic was especially evident within the City of Austin, where transaction volume declined 7.1%, but prices edged down by only 1.5%. These figures suggest core urban home values have remained relatively stable, with inventory being absorbed primarily through slower transaction pace rather than sharp price reductions.

As inventory continues to accumulate and time on market extends, the underlying mechanics of transactions across the Greater Austin MSA are shifting. Sellers are no longer focused solely on whether to make concessions, but increasingly on how to structure pricing, timing, and terms in a way that can realistically lead to a closing. At the same time, buyers are operating more deliberately, placing greater emphasis on fair pricing and property fundamentals rather than broadly bidding up available listings.

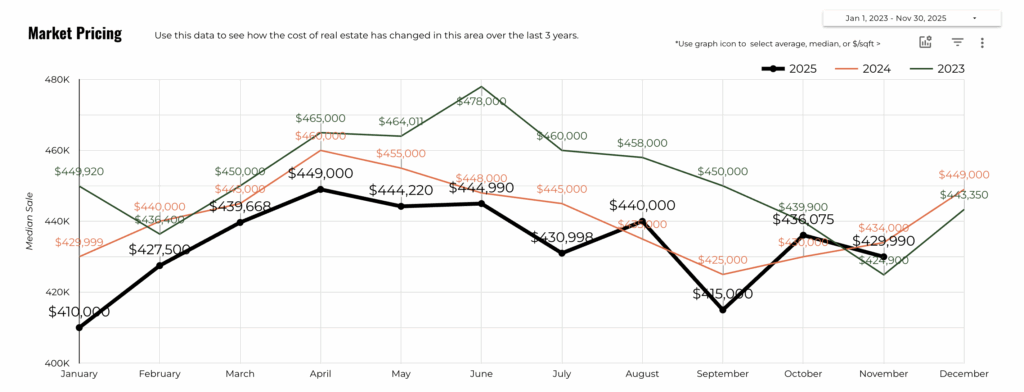

Pricing and Sales Activity

In November, the median sales price across the Greater Austin region reached $429,900, down 1.1% year over year, reflecting overall price stability rather than a sharp correction. Closed sales volume declined 15.9%, underscoring a more cautious buyer environment and longer decision cycles.

One notable counterpoint was pending sales, which increased 4.5% year over year to 2,269 contracts. This indicates that underlying demand remains present, though buyers are proceeding more selectively and taking additional time before committing.

Looking at surrounding areas, most counties experienced price adjustments. Hays County stood out as one of the few markets where pricing remained supported, with median prices rising 6.9% year over year. However, transaction volume fell significantly, suggesting that buyer activity has become more concentrated, with sales occurring primarily among a smaller subset of well-positioned homes.

Listings and Inventory

On the supply side, new listings declined 3.1% year over year in November, reflecting a slower pace of seller participation amid current pricing and demand conditions. Meanwhile, active listings increased 11.2%, pushing months of inventory to 6.3 months. Average days on market rose to nearly 80 days, indicating expanded negotiation leverage for buyers.

Among individual counties, Bastrop and Caldwell showed the most pronounced inventory pressure, with months of supply reaching 7.2 and 6.1, respectively. In both markets, prices and transaction volume faced pressure simultaneously, making these areas among the most competitive environments for sellers at present.

Rental Market

The rental market in November remained broadly stable but continued to soften at the margin. Median rents declined 2.3% year over year to approximately $2,100, while closed lease volume fell 13.2%, reflecting more cautious tenant decision-making amid increased supply. New rental listings declined across the region, mirroring trends seen in the for-sale market, as some landlords opted to delay listings or take a wait-and-see approach.

This combination of slower leasing activity and supply restraint was particularly evident within the City of Austin. Rents remained relatively stable, but leasing volume declined by approximately 13%. New rental listings fell 7.9%, pending leases softened, and properties spent more time on the market.

Takeaways for Buyers and Sellers

- For buyers, the current environment places greater emphasis on selecting the right asset rather than rushing into a purchase. Rising inventory, stable pricing, and expanding negotiation room offer a more disciplined entry point for those focused on fundamentals.

- For sellers, despite slower transaction counts, pricing has held firm and demand remains steady across most submarkets. Proper pricing, thoughtful preparation, and strong presentation remain essential. Homes that are well-maintained and competitively priced continue to attract committed buyers and achieve successful outcomes.

Whether you’re looking to buy, sell, or invest, our Real International team is here to deliver tailored strategies to help you succeed in today’s market.

👉 Contact us today at info@realinternational.com to uncover opportunities in the Austin.