This article gives balanced, data-driven look at macroeconomic shifts and analyzes October leasing and sales activity across major areas in the Austin-Round Rock-San Marcos Metropolitan Statistical Area (MSA).

(Note: All housing market charts are sourced from Unlock MLS. Due to slight differences in reporting periods and geographic coverage, minor discrepancies in numbers may exist. Please focus on overall trends and market structure when interpreting these signals.)

Macroeconomic Snapshot

The macro environment in October was shaped by an unusual backdrop. A federal government shutdown lasting more than six weeks disrupted the Bureau of Labor Statistics’ normal data collection schedule. As a result, the White House signaled that the October job report and October CPI may not be released as planned, and may not be published at all.

Toward the end of October, the Federal Reserve announced a reduction of the benchmark rate to 3.75%-4.00%, highlighting in its statement that overall economic activity continues to grow moderately and that labor market has weakened. The Fed emphasized that policy direction in the coming months will depend heavily on incoming data once regular reporting resumes.

At the same time, mortgage rates continued a gentle downward drift. The 30-year fixed rate hovered in the 6.1%-6.2% range, a modest decline but still notable given the elevated levels seen earlier this year. For the housing market, this easing translated more into sentiment improvement than into a measurable increase in activity. October followed the typical seasonal pattern of slower fall activity, with buyers and sellers moving at a steady, deliberate pace rather than accelerating into the new rate environment.

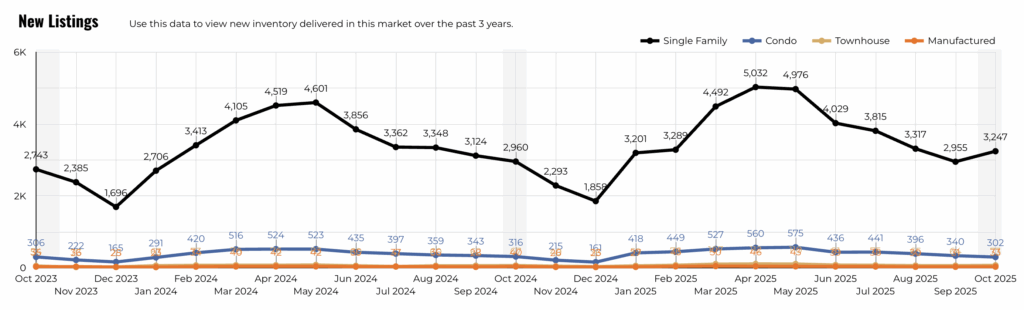

Austin Metro Housing Landscape

The Austin metro area extended its usual autumn cooldown in October, though several indicators showed meaningful shifts beneath the surface. Prices demonstrated renewed resilience, inventory levels continued to rise, and a few local submarkets displayed particularly sharp movements. While total closed transactions declined year over year, higher median prices and increased listings suggest that the region is gradually moving toward a more balanced, opportunity-rich environment for buyers and sellers as we enter the final stretch of 2025.

Pricing and Sales Activity

Although closed sales dropped 9.6% metro-wide, median sales price reached $439,000, up 1.4% year over year and broadly consistent with this year’s stable pricing band.

However, one notable bright spot emerged in new under contract, which rose 5.8% to 2,463, indicating that buyers remain active, though more selective in timing and property choice.

Among local areas, the City of Austin stood out as one of the few markets where median price, closed sales, and total sales volume all increased year over year—a sign of relative stability and renewed demand in the urban core.

At the opposite, Caldwell County saw the sharpest decline in the metro. Median prices fell more than 10%, and closed sales dropped by nearly half.

Listings and Inventory

New listings rose 7.9%, while active listings increased 12.4% year over year. Months of inventory expanded to 5.3 months, up 0.5 months from last year, continuing the metro’s steady move toward a balanced market.

The combination of rising listings and higher pending sales may help sustain transaction levels through the holiday season, even as overall activity typically slows.

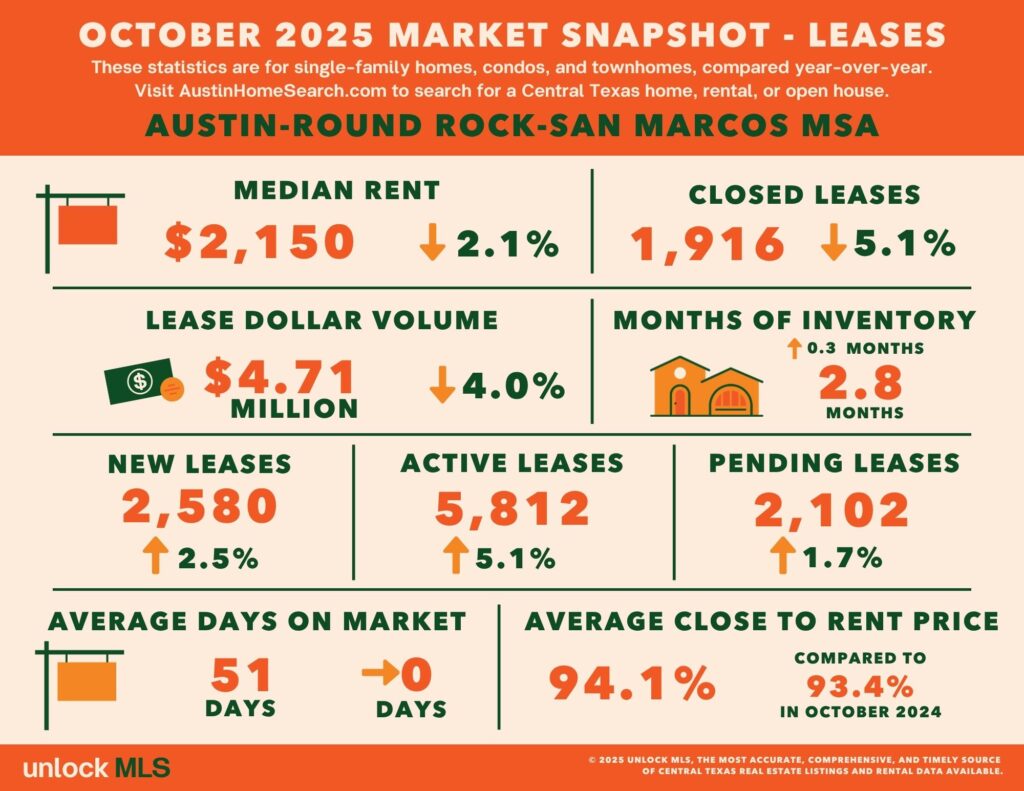

Rental Market Conditions

The rental market remained broadly stable in October. The metro-wide median rent was $2,150, a modest 2.1% decline year over year. Closed leases fell 5.1%, while both new rental listings and active rental supply increased, signaling a tenant-favored environment characterized by ample availability and heightened competition.

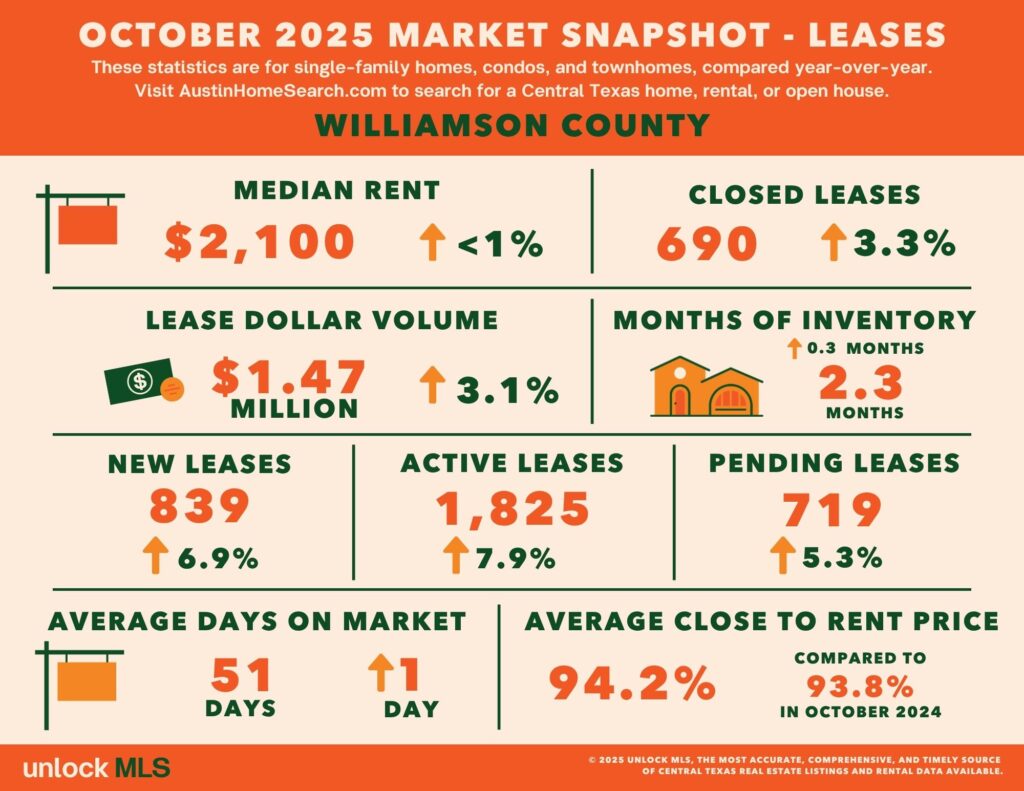

Across submarkets, central Austin remain higher rent levels but leasing activities slowed, prompting many renters to compare alternatives in surrounding counties. Williamson County and Bastrop County demonstrated particularly resilient demand. Bastrop’s rental activity was the most dynamic in the region, with pending leases up nearly 20% and new listings also showing double-digit gains.

Williamson County, meanwhile, showed steady and reliable demand. Both closed leases and total lease volume increased year over year, making it the most stable rental submarket in North Austin. Bastrop and Williamson thus reflected two different but healthy profiles: “active growth” versus “steady strength.”

Takeaways for Buyers and Sellers

- For buyers, fall and winter provides greater selection, less competition, and a calmer negotiation environment. With mortgage rates easing and the potential for further adjustments in 2026, now is a strategic moment to evaluate options before renewed competition returns.

- For sellers, despite slower transaction counts, pricing has held firm and demand remains steady across most submarkets. Proper pricing, thoughtful preparation, and strong presentation remain essential. Homes that are well-maintained and competitively priced continue to attract committed buyers and achieve successful outcomes.

Whether you’re looking to buy, sell, or invest, our Real International team is here to deliver tailored strategies to help you succeed in today’s market.

👉 Contact us today at info@realinternational.com to uncover opportunities in the Austin.