Almost every professional knows that contributing to a 401(k) or traditional IRA is a smart way to reduce their tax burden. What most don’t realize, however, is that your retirement capital does not have to remain trapped in the volatile, unpredictable swings of the stock market.

Imagine deploying those exact same retirement funds to acquire a residential property right here in the high-growth Austin market, or investing them directly into premium commercial real estate developments. Now imagine that every dollar of rental income, quarterly project distributions, and future capital gains flows back into your account 100% tax-free or tax-deferred.

This is the exact strategy used by institutional investors and high-net-worth individuals to build multi-generational wealth. The vehicle behind this financial game-changer is the Self-Directed IRA (SDIRA).

Here is a look at how sophisticated investors use this advanced tool to achieve unparalleled financial leverage.

The Golden Cage of Traditional Retirement Accounts

When you open a standard IRA with a mainstream brokerage or participate in a corporate 401(k) plan, your investment options are quietly restricted. You are usually confined to a pre-selected “menu” of mutual funds, stocks, and bonds.

Traditional brokerages build their entire business model around transaction fees and the continuous trading of paper assets. Because investors are systematically conditioned to look only at Wall Street, many fall into a cognitive blind spot, assuming retirement capital cannot exist outside of a brokerage account.

The downside? When the market faces a correction or enters a period of high volatility, investors have no choice but to ride the roller coaster, lacking any tangible, hard assets to act as a macroeconomic hedge.

Complete Autonomy

A Self-Directed IRA changes the rules of engagement. Structurally, an SDIRA holds the exact same legal and tax status with the IRS as a standard IRA. The fundamental difference lies in the complete transfer of investment control back to you.

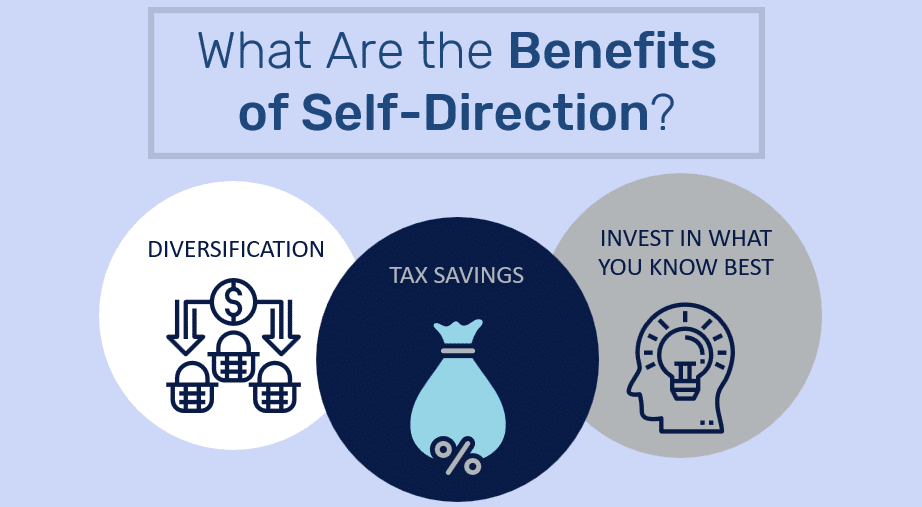

Barring a few explicit statutory exclusions enforced by the IRS, an SDIRA empowers you to diversify your capital into alternative, inflation-resistant hard assets. And among these alternative assets, real estate stands as the most mature, historically proven cornerstone.

The Hardcore Advantages of Alternative Real Estate SDIRAs

For investors focused on defensive wealth preservation and aggressive tax optimization, utilizing an SDIRA for real estate projects offers two non-negotiable advantages:

1. Ultimate Tax Shielding

- The Tax-Deferred Play (Traditional SDIRA): Imagine your SDIRA acquires an investment property or backs a major commercial development. Every monthly rent check, every quarterly dividend, and the six-figure capital gains realized upon the ultimate sale of the asset incur zero immediate tax liability. 100% of the returns stay inside the account, compounding exponentially year after year, untaxed until you begin making eligible withdrawals in retirement.

The Tax-Free Play (Roth SDIRA): This is where the wealth-building potential truly accelerates. While contributions to a Roth SDIRA are made with after-tax dollars, all future rental yields, project distributions, and equity appreciation are 100% tax-free for life. This structural design can easily save you hundreds of thousands of dollars in capital gains taxes over the lifecycle of your real estate portfolio.

2. Activating Dormant Retirement Capital

Over the course of a career, it is common to accumulate a fragmented trail of retirement accounts, an old 401(k) from a previous employer, a forgotten traditional IRA, or a small business retirement plan. Because managing these individual accounts takes time and effort, this capital frequently sits passive and underutilized in default mutual funds.

Through a compliant Direct Rollover, you can consolidate and transfer these dormant funds into a single, cohesive SDIRA. Done correctly, this institutional transfer triggers zero tax penalties and zero immediate tax liabilities, instantly transforming stagnant paper numbers into the down payment for a physical property or the initial capital for a premium real estate syndication.

The Built-In Asset Firewall

Beyond the clear tax advantages, structuring your investments through an SDIRA introduces a sophisticated layer of legal defense.

When you purchase real estate or take an equity position in a development project through an SDIRA, the asset’s legal title or equity shares are held directly under the name of your SDIRA custodian, rather than your personal name. This creates a distinct legal separation between your personal liability and your retirement wealth.

The Texas Advantage: Under Texas’s robust asset protection and homestead framework, assets securely insulated within a qualified retirement structure are exceptionally well-shielded from personal or external business liabilities, ensuring your hard-earned wealth remains protected.

Who Can Leverage an SDIRA?

A common misconception is that the barrier to entry for an SDIRA is exceptionally high. In reality, the account structure is highly accessible. You can establish a Self-Directed IRA if you match any of the following profiles:

You hold an existing Traditional or Roth IRA.

You are self-employed, a freelancer, or run a side business (qualifying you for small business structures like a SEP IRA or Solo 401(k)).

You have an idle 401(k) or 403(b) account sitting with a previous employer.

Navigating the Compliance Boundaries

As an advanced, IRS-sanctioned financial instrument, the SDIRA operates within precise regulatory boundaries. To preserve your tax-exempt status, the movement of funds must remain entirely self-contained within the account silo, and you must maintain a strictly passive investment posture.

Because navigating these nuances requires precision, aligning yourself with an experienced investment team backed by a vetted compliance ecosystem is essential.

If you would like to learn more about this powerful tax saving tool, reach out today! We are ready to help you unlock the full wealth-building potential of your retirement portfolio.