The Federal Reserve delivered its third rate cut of 2025, lowering the federal funds rate by another 25 basis points to a target range of 3.50%–3.75%. The move was widely expected, but what happened inside the Federal Open Market Committee (FOMC) was not. This meeting produced the sharpest internal split of the year, offering a clearer signal about the uncertainty shaping the year ahead.

While the rate cut itself was uncontroversial for markets, the vote revealed growing disagreement within the Fed: two policymakers opposed further easing, arguing that inflation progress was not yet sufficient, while one member favored a larger 50-basis-point cut, warning of rising risks in the labor market. This divergence underscores a fundamental shift. It’s no longer simply about whether the Fed will cut, but how much, how quickly, and how confidently.

(source: Fox Business)

(source: Fox Business)

Chair Jerome Powell emphasized this tension in the post-meeting press conference. Inflation has cooled meaningfully from earlier in the year, but it remains above the Fed’s 2% target. At the same time, the labor market has softened more noticeably: job gains over the past three months averaged just 29,000, a striking slowdown from the first half of the year. Powell described the decision as a “risk-management” cut designed to cushion emerging weakness, rather than a reaction to recession-level conditions. He also reiterated that the future path of policy will remain entirely data-dependent.

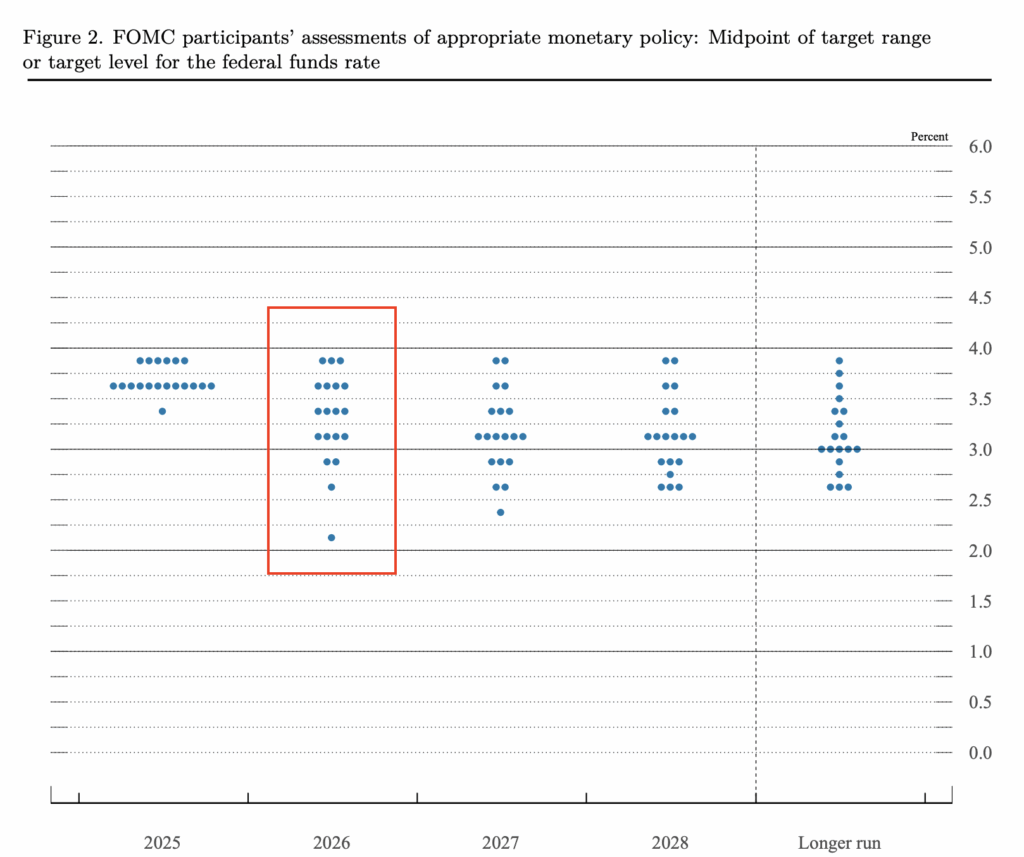

Alongside the rate decision, the Fed released its updated dot plot, offering the clearest picture yet of what policymakers expect in 2026. The new projections show that most officials anticipate only one more rate cut next year, bringing the median forecast for 2026 to roughly 3.4%. In other words, after a year of more aggressive easing, 2026 is expected to be slower, more cautious, and far less predictable. The committee remains divided on how quickly inflation will return to target and how much additional policy support the economy may ultimately need.

(source: Federal Reserve, FOMC Projection Materials)

(source: Federal Reserve, FOMC Projection Materials)

This uncertainty lands at a sensitive moment. Powell’s current term as Fed Chair expires in May 2026, and as his leadership enters its final stretch, the widening range of views inside the committee adds another layer of complexity to how markets interpret the Fed’s longer-term direction.

Mortgage Rates: Gradual Relief, Not an Immediate Drop

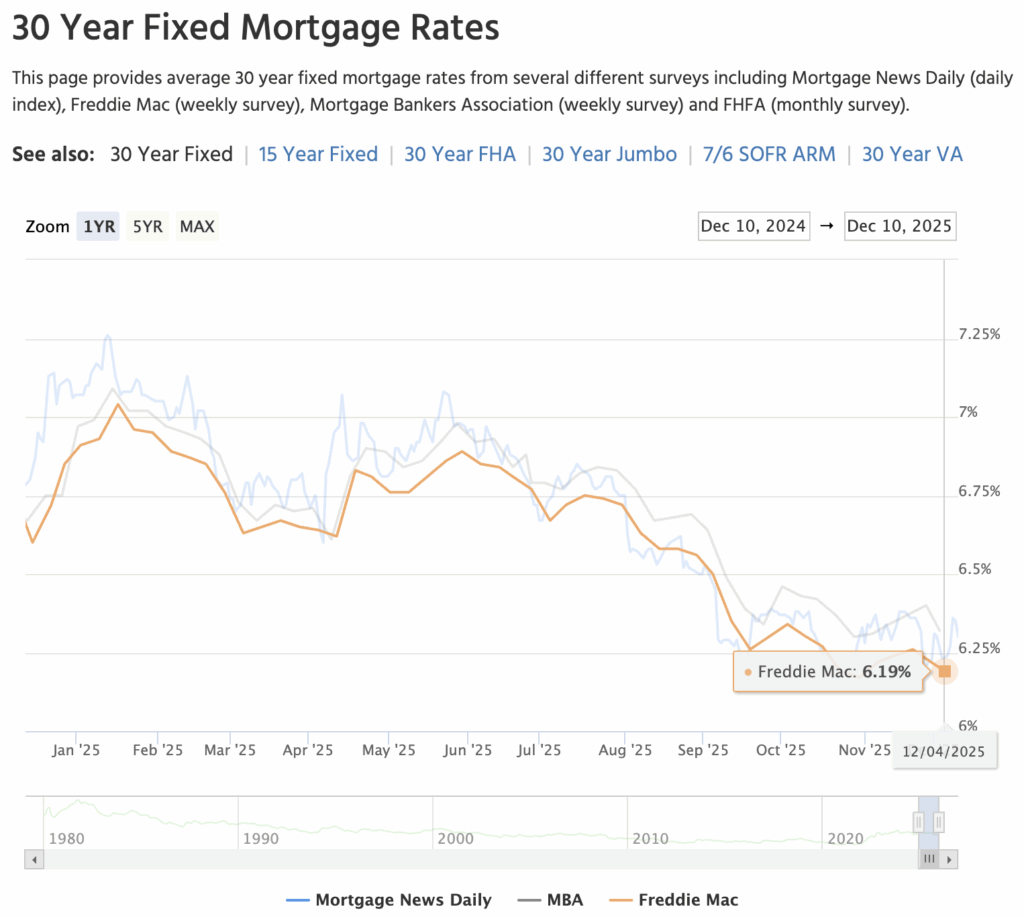

For investors, the most practical question following any Fed decision is how quickly rate cuts translate into lower mortgage borrowing costs. The answer this time: not immediately.

The federal funds rate and mortgage rates do not move in lockstep. Mortgage rates are driven primarily by longer-term Treasury yields, especially the 10-year, rather than the Fed’s short-term benchmark. According to CNBC, markets had already priced in this 25-basis-point cut well before today’s decision, meaning the announcement itself did little to shift mortgage rates in the short term.

(source: Mortgage News Daily)

(source: Mortgage News Daily)

But directionally, the picture is changing.

With financial markets gradually adjusting to a more accommodative stance, long-term borrowing costs are likely to drift lower over the coming weeks and months, even if the path isn’t linear. This makes the Fed’s decision less of an instant discount and more of a signal that the broader rate environment is finally turning a corner.

This makes the Fed’s decision less of an instant discount and more of a signal that the broader rate environment is finally turning a corner.

What This Means for Investors

For investors, the implications of this rate cut are becoming clearer, not because the cut was large, but because it confirms a shift in trajectory.

1. Financing conditions are improving.

As long-term yields ease, financing costs move lower, reducing carrying pressure and reopening opportunities for refinancing. Mortgage rates hovering around 6.1%–6.3% are already markedly below their peaks earlier this year, and the trend still points gradually downward.

2. Buyer confidence is turning before prices do.

Rate relief, even gradual relief, has a psychological effect. Confidence typically recovers earlier than transaction volume or pricing, and we are beginning to see the early signs of that shift. Demand doesn’t snap back overnight, but it does start to re-enter quietly and steadily.

3. Negotiation leverage may tighten sooner than expected.

As confidence returns and buyers re-engage, well-priced and high-quality homes will be absorbed more quickly. The window for strong negotiation leverage, which has characterized much of the market this year, may begin to narrow as competition picks up.

The Bottom Line

The rate cut itself wasn’t the headline: the shift in direction was. With internal divisions rising and only one cut expected next year, policy will move more cautiously. Mortgage rates won’t react immediately, but the broader trend points toward gradually improving conditions.

With year-end here, several major builders are offering limited-time rate promotions. Real International now have exclusive opportunities available.

📧Contact us to learn more: info@realinternational.com.