In our previous article, we discussed how a Self-Directed IRA (SDIRA) allows you to break free from traditional market limitations. By transitioning volatile retirement funds into tangible, inflation-resistant real estate, you can lock in steady cash flow and long-term appreciation while maximizing your tax benefits.

The feedback was clear: investors are highly driven to protect their hard-earned wealth and let it compound entirely shielded from tax erosion. In today’s unpredictable macroeconomic environment, a strategy that offers both robust asset protection and massive tax optimization is invaluable.

However, the IRS does not grant these extraordinary tax advantages without strict conditions. To safeguard your wealth, you must play strictly by their rules. Using your retirement capital to invest in real estate requires a completely different mindset than traditional, hands-on property ownership.

Today, let’s look at the two critical real estate SDIRA pitfalls investors face, and how you can navigate them to ensure your tax-advantaged returns land safely.

Pitfall 1: Failing to Maintain an “Arm’s Length”

When it comes to SDIRA real estate investments, the IRS enforces one core commandment: the Arm’s Length Transaction rule.

Legally, your retirement account is treated as one distinct entity, and you, as an individual, are treated as another. There must be a strict, physical arm’s distance between the two, meaning no overlapping personal interests, benefits, or transactions are permitted.

![]()

During the property ownership phase, beginners often accidentally cross these three distinct red lines:

Red Line 1: Self-Dealing. Neither you, your spouse, your parents, nor your children can ever reside in, use, or lease the property, even for a single day. It must remain a strictly commercial, investment-only asset.

Red Line 2: Providing “Sweat Equity.” If a pipe leaks or a wall needs remodeling, you cannot fix it yourself. You cannot contribute personal labor to your own IRA asset. All management, maintenance, and repairs must be handled and invoiced by an unrelated, third-party professional team.

Red Line 3: Commingling Funds. Property taxes, insurance, and maintenance costs must be paid 100% directly from your SDIRA account. You cannot pay with a personal credit card and reimburse yourself later. Conversely, all rental income and distributions must flow directly back into the SDIRA, never sitting in your personal bank account.

![]()

The Silver Lining: Becoming a Passive Investor by Design

At first glance, these rules might seem encumbering. You might wonder: Is investing retirement funds into real estate worth the constant compliance oversight?

In reality, sophisticated investors view these restrictions as a major structural benefit. Because the IRS legally bars you from active management, it practically forces you into the ultimate hands-off, passive investment model.

There are two primary ways to execute this seamlessly:

Path A (Direct Property Ownership): You outsource 100% of the operational legwork to an established local property management company. From tenant vetting to midnight plumbing calls, they handle everything and settle bills directly with your SDIRA custodian. You simply track your compliant, passive returns from your phone.

Path B (Real Estate Syndications & Funds): You deploy your SDIRA funds directly into institutional-grade real estate development projects or private equity funds. Structurally, you act strictly as a Limited Partner (LP). You have zero operational responsibilities, and the project sponsors distribute tax-free returns directly back into your custodian account, reducing your compliance risk to virtually zero.

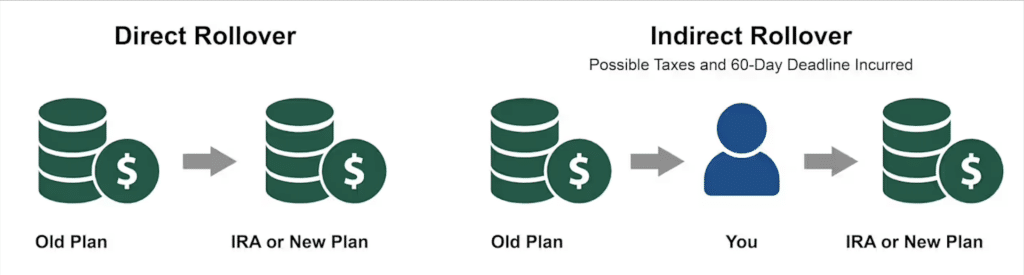

Pitfall 2: Touching the Money During the Transfer

While the “Arm’s Length” rule governs the holding phase, an even costlier mistake often happens right at the starting line when moving idle retirement capital, such as an old 401(k) or a traditional IRA.

When investors decide to diversify into real estate, their first instinct is often to have their current brokerage liquidate the account and mail them a check, intending to use those funds to buy the property or invest in a project.

This is a critical misstep. The moment those funds land in your personal checking account, the IRS flags it as an early distribution. If you are under the age of 59.5, you will trigger severe financial consequences:

An automatic, non-negotiable 10% early withdrawal penalty.

The entire transferred amount will be treated as ordinary income for that fiscal year, subjecting it to heavy, immediate personal income taxes.

A single unguided maneuver can cause a massive chunk of your wealth to evaporate before it ever enters the real estate market.

The Professional Standard: Direct Rollovers

In professional wealth management, the golden rule of moving retirement capital is simple: the money never touches your hands.

Instead, we utilize a Direct Rollover. This establishes a secure, compliant bridge between your newly opened SDIRA custodian and your previous account administrator. The capital moves seamlessly from institution to institution.

Because you never take personal possession of the money, the entire transfer triggers 0 penalties and 0 immediate taxes. Your capital remains 100% intact, fully optimized to capture the high-defense advantages of premium real estate assets.

As a specialized tax optimization tool, a Self-Directed IRA offers incredible financial power, but its execution requires meticulous attention to detail. A single administrative misstep can result in severe IRS penalties and unnecessary capital erosion.

Feel free to email us. We are happy to help you map out the compliant workflow and introduce you to trusted resources.

Disclaimer: This article is for informational and educational purposes based on real estate market experience. Real International is a real estate investment consulting firm, not a licensed CPA, tax attorney, or financial advisor. This content does not constitute, nor replace, professional tax, legal, or financial advice. Please consult with your CPA or tax professional before initiating any SDIRA transactions.